Table of Contents

What is the 60/30/10 rule budget?

If you want to get serious about saving for retirement or paying off your debt, then you might want to implement the 60/30/10 rule budget into your financial strategy.

This straightforward budgeting method focuses heavily on savings and debt payoff, and can help you reach your budget goals faster than other spending plans.

In this post, I’ll go over exactly what the 60/30/10 rule budget is, how to use one with your finances, and if it’s the right strategy for you.

Here’s what you should know about this simple but effective budgeting plan.

Grab this FREE 60/30/10 rule budget template, and start crushing your money goals fast!

How does the 60/30/10 budget rule work?

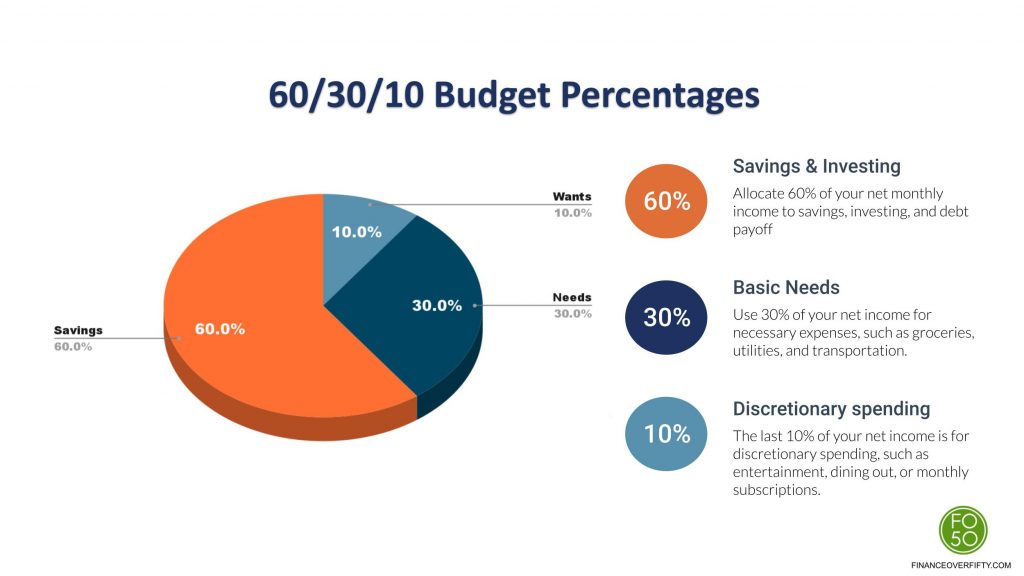

The 60/30/10 rule budget uses 3 categories of spending to manage your finances. The specific percentages are used to determine what portion of your current income will be applied to which category.

First, 60% of your after-tax income will be dedicated to savings, investing, or debt payoff.

Second, 30% will go toward necessary expenses for daily living. This includes your mortgage or rent, utility bills, food budget, insurance, transportation, etc.

Third, 10% is for discretionary spending, such as entertainment, travel, and hobbies.

As you can see, this 3-fold breakdown is a budgeting solution that could really simplify your money management. It is also highly effective at helping you reach your savings, investing, and debt reduction goals.

Who should use the 60/30/10 rule budget?

The 60/30/10 budgeting rule prioritizes financial goals over spending. Because of the large percentage allocated to savings or debt payoff, it’s not a budgeting style that is suited to everyone’s circumstances.

For example, if you are just starting your first budget, I don’t recommend this method for you. You’ll be better off with a zero-based budget that has a high degree of accountability for every single dollar of income. Although it is a more complicated budget, you’ll be able to have more control of your money management. (For more info, ready my complete guide on the zero-sum budget method.)

Also, if you’re struggling with making ends meet and live a paycheck to paycheck lifestyle, you should pick a budget strategy that allows for a higher percentage of household expenses. Your priority is to make sure you’re covering your bills, not stashing most of your income away for retirement.

However, if you have been budgeting for a while and you’re ready to shift your financial priorities toward saving more and paying off your debt, then you should definitely consider this ambitious strategy.

Or, if you have a major financial goal you want to reach as fast as possible, this budgeting rule can help you achieve it.

Allocating over half of your take-home pay toward savings and debt will require you to cut some expenses and lower your discretionary spending. Before you apply this budgeting approach to your own finances, be sure you’re willing to make the sacrifices it requires.

What are the pros and cons of the 60/30/10 budget rule?

As with all budgeting methods, there are advantages and disadvantages to the 60/30/10 rule. Let’s go over what those are.

Benefits of the 60/30/10 budgeting rule

One of the greatest benefits of this strategy is its simplicity. You don’t have to be concerned with how you spend every dollar like the zero-sum budget. Instead, you only need to be concerned with three percentages, which means you’re only dealing with three categories.

As long as you can keep track of your three categories, the 60/30/10 rule is easy to implement.

Another benefit to this ambitious spending plan is its effectiveness in achieving financial objectives quickly. This is especially important for those who are behind on their retirement savings, have no emergency fund, or need to get out of debt fast.

A third advantage of this strategy is it will help you to control spending habits that are wasting your income. You will need to be very diligent and selective about how much you spend on unnecessary items. You may also need to get creative with decreasing your household expenses. Both practices will teach you what your money values truly are.

Lastly, the point of using this budgeting method is so that you will eventually have more in savings, a thriving portfolio, and no debt. Those are all very profitable benefits to using the 60/30/10 rule budget.

Disadvantages of the 60/30/10 rule

As mentioned before, this budget is not the best choice for everyone. It’s a challenging method to maintain, and may seem too restrictive for some.

One downside is you’ll have less to spend on the fun stuff – like eating out with friends, going on vacations, buying new clothes, etc. This may be a huge adjustment to your current lifestyle and spending habits – possibly one you’re not willing to make.

You may also discover that you have to find ways to cut your household expenses. If your rent payment alone takes up almost 30% of your take-home income, are you willing to move to more affordable housing? The sacrifices you need to make might be too high.

Another downside to this method is that it’s very difficult for someone on a low income. If you can save over half of your take-home pay, then obviously you are not struggling financially with all of that extra discretionary income. But, for someone barely covering the bills, this percentage method may be impossible to apply.

Also, if you need more details to manage your money well, then you will likely find the 60-30-10 method frustrating. With only three categories to track, there can be a lot of “gray” areas and you won’t have the more structured budget you desire.

How to set up a 60/30/10 budget for more savings

Setting up a 60/30/10 budget for your own finances is very straightforward:

- Calculate the total amount of your monthly after-tax income.

- Determine the dollar amount for each percentage category: 60%, 30%, 10%

- Confirm that you can cover your necessary monthly expenses with 30%.

- Decide if you’re willing to reduce your discretionary spending to 10%.

- Allocate your income to each category every month.

Let’s go over each step in detail.

Step 1: Add up your total monthly take-home pay

This is where it all starts.

Your monthly take-home pay is what you receive after all taxes and deductions are taken out. Be sure you include all income sources (employment income, side hustles, dividends, child support or alimony, any inconsistent income, etc.).

If you have an hourly job, get overtime, or receive some type of quarterly or biannual income, then your monthly after-tax income will vary. No matter how much you bring in each month, you’ll apply the same percentages in your budget.

Here is an example:

- Monthly take-home pay from full-time job = $5,500

- Monthly net income from side hustle = $500

- Monthly child support = $1,000

Total of all income streams = $7,000

Step 2: Divide your total net income into 60%, 30%, and 10%

Once you have the total of your monthly net income, calculate each percentage.

Using the example in step 1, this would be the breakdown of your net monthly income:

- $7,000 x 60% = $4,200

- $7,000 x 30% = $2,100

- $7,000 x 10% = $700

Step 3: Confirm that 30% can cover your necessary expenses

Once you know the dollar amount of each percentage category, you’ll need to decide if 30% is enough to cover your necessary expenses.

These expenses are non-negotiable. Here is a list of possible basic expenses you’ll need to cover every month:

- Housing costs (mortgage payment or rent)

- Groceries

- Insurance

- Utilities

- Basic clothing

- Transportation costs

- Child care expenses

- Minimum debt payments (any additional debt repayments would go into the debt repayment bucket)

Add up your monthly necessary expenses to confirm they are equal to or less than 30% of your take home pay. If they aren’t, you’ll need to lower some of those expenses before you apply the 60/30/10 rule budget to your finances.

Step 4: Determine if you’re willing to reduce discretionary spending to 10%

You may be a little shocked at how limiting a 10% discretionary budget amounts to, so it’s important to determine if you’re willing to make some sacrifices.

Some “extra” expenses you may want to spend this money on could be:

- Entertainment (movies, concerts, etc.)

- Dining out

- Additional clothing

- Vacations

- Hobby expenses

- Subscription fees (gym membership, streaming services, etc.)

- Recreational activities

Use a budget tracker to record your spending for 30 days to get a good idea how much you currently spend on unnecessary purchases. How much do you spend on eating out, new clothes, going to the movies, etc? Compare this number to your 10% amount, and decide if it’s a limit you’re willing to commit to.

Step 5: Allocate the percentages to each category

After you’ve done all of the calculations, it’s simply a matter of sticking to your new budget. You can do this a number of ways, but setting up automatic transfers for every income source can be very effective.

Depending on the financial goal you’re trying to reach, there are a variety of ways to ensure you achieve it.

- For a big savings goal, open a separate account to deposit 60% into your savings category.

- For investing into retirement savings, open a 401(k) or IRA. For a 401(k) through your employer, set up a direct deposit into the account. However, don’t take out 60%, because this would be pre-taxed. Instead, figure out what percentage of your gross income would equal 60% of your take home pay. Using the example above, if your gross paycheck is $9,000, you’ll want to request 47%, which would deposit about $4,200 into your 401(k). If you open an IRA, you can make contributions either pre- or post-tax.

- To pay off debt, make a payment equal to 60% of your income every time a deposit goes into your account.

- It’s possible you have multiple budgeting goals – like, saving for a down payment, increasing your retirement fund, and paying off your credit card debt. In this case, simply divide the 60% between the three.

- Use 30% of your after-tax income to pay your monthly bills. You might find that 30% doesn’t stretch very far, so consider finding ways to decrease your basic expenses. For example, you could lower your insurance premiums with a higher deductible, or decrease your mortgage payment by refinancing with a lower rate.

- The 10% that’s left is for you to spend at your discretion – so choose wisely!

Once you’ve set up your percentage structure and budget allocations, it’s just a matter of sticking to your spending plan!

Why should I use 60% of my paycheck for savings or debt?

Developing the money habit of saving allows you to enjoy a degree of financial freedom.

With a little extra money in the bank, you can meet unexpected expenses without relying on debt. You experience less stress just knowing you’re financially prepared for emergencies. You also have the freedom to cover costs that enrich your life, like going on a vacation, paying for your daughter’s wedding, getting a new car, etc.

Also, getting out of debt and building sufficient savings are both critical steps to reaching financial freedom before you retire. Applying 60% of your income would be a great way to reach those goals faster, especially if you’re behind with your retirement fund.

However, saving over half of your income is a unique and ambitious goal. But, if you’re serious about achieving your financial objectives, you can reach them quickly with this budgeting method.

Here are a few reasons to save 60% of your income:

- Pay off your mounting credit card bills

- Build a 6-month emergency fund

- Catch up on your retirement savings

- Save up for a 20% down payment for a house

- Start your own business

- Invest in real estate for passive income

- Open a college savings fund for your teenager’s college tuition

How you can make the 60/30/10 rule work for your finances

The 60/30/10 budgeting strategy has a strong emphasis on savings and debt reduction. If these two results are the goals you’re shooting for, you can make this budget work for you.

The first step is determining if 30% of your income will effectively cover your basic expenses. For many people, housing costs alone eat up 30% of their paychecks. This is when you need to get a little creative with lowering your bills.

One option to significantly decrease your housing expenses is to refinance your mortgage with a lower rate. This alone could potentially lower your monthly bill by a couple hundred dollars. If you’re a renter, you may have to move to a less expensive area where rent fees are cheaper.

You’ll also need to be content with less discretionary spending. This could look like having more home-cooked meals instead of dining out, or shopping at thrift stores instead of Target for a new outfit.

The bottom line is that the 60/30/10 rule budget may require a serious lifetime adjustment on your part. You’ll need to decide if your savings goals are worth making these sacrifices for.

Can you realistically follow the 60/30/10 rule for money?

Paying off all of your debt or maximizing your retirement fund sound like some pretty awesome goals. After all, who doesn’t want more money and less debt?

But, not everyone is able to apply this spending plan to their finances. For someone living a paycheck to paycheck lifestyle, this budget method wouldn’t be possible.

If you want to be realistic about following the 60/30/10 rule budget, you’ll need to make enough money that allows you to effectively live off 40% of your net income.

You might already be in this position but not realize it. If you spend a lot on unnecessary expenses, you may be able to significantly lower those costs and start applying more toward savings.

Track your spending for 30 days to see how much wiggle room you have with your income. This will give you a clearer idea if the 60/30/10 budget is realistic for you.

Even if you discover that this budget method wouldn’t work for you currently, you can make the effort to increase your income. Maybe you only need a few hundred dollars a month of additional income to make it work for you. You could easily make up for this deficiency by getting a part-time job or weekend side hustle.

You could even make adjustments to this budgeting method to make it more well-suited for your financial situation. Consider changing the percentages so they are easier for you to apply. For example, maybe a 50/30/20 budget would be better for your circumstances.

Don’t give up on your financial goals just because you don’t have the means right now to achieve them. Take the initiative to generate more income and lower your expenses – even if just temporarily – so you can reach your savings goals faster.

A 60/30/10 budget example

Now that we’ve gone over many of the details for this budget plan, let’s look at an example.

Let’s say you have 3 income streams that net an annual income of $60,000. This amount represents your income after taxes and deductions have been taken out.

If you divide this total by 12, you’ll get an average monthly net income of $5,000.

Therefore, your budget breakdown would look like this:

- 60% = $3,000

- 30% = $1,500

- 10% = $500

Now, you can budget your spending for each percentage category.

If you are diligent with keeping this budget method, you will be able to apply $36,000 of your income to savings and/or debt within one year.

That’s a huge increase toward meeting your financial goals!

Use the 60/30/10 Budget Calculator

Wondering what these percentages would be for your own finances?

Plug in your estimated total net income, and this 60/30/10 budget calculator will tell you.

Use the 60-30-10 budget template

So, are you ready to put the 60/30/10 budget in action?

If so, download this free budget worksheet and start saving more today!

Other methods for budgeting by percentages

Personal finances are personal. That means you get to decide the best way to budget your income.

If the 60/30/10 budget rule seems too extreme for your current financial circumstances, try a different budget method based on other percentages.

Here are six common budgeting methods to choose from:

70-20-10 budget rule

The 70-20-10 rule uses a budget allocation that applies the majority of your take-home pay to expenses instead of savings:

- 70% for all expenses, both necessary and discretionary

- 20% for savings or debt repayment

- 10% for investing or charitable giving

This is an effective budget for those who have higher living costs and lower debt.

60-20-20 budget method

Here is another budget based on different percentages that could help you manage your finances better and help you reach your goals.

The 60-20-20 budget allocation dedicates the majority of your net income to your necessary living expenses:

- 60% for necessary costs, like housing and food budget

- 20% for financial goals, living building an emergency fund or investing for retirement

- 20% for all discretionary spending

If you have high housing costs or a large family to support, this method could be a good option for you.

50-20-30 rule budget

The 50-20-30 rule for budgeting was created by Senator Elizabeth Warren. This popular budgeting method keeps your essential expenses down to half of your total net income:

- 50% for needs

- 30% for wants

- 20% for savings and debt reduction

Again, another good option that allows more for daily living expenses and a smaller percentage for savings.

30-30-30-10 budget method

This more in-depth budget method divides your net income into 4 percentage categories:

- 30% for housing expenses (mortgage, rent, HOA fees)

- 30% for essential costs (food budget, insurance premiums, utilities, etc.)

- 30% for savings and debt repayment

- 10% for discretionary spending

This is a well-balanced budget plan that would keep you from overspending on unnecessary purchases.

80/20 budget

This percentage budget method only has two categories for your net income:

- 80% for all expenses

- 20% for savings

This is a very simple, but effective, spending plan that is easy to implement. All you have to do is set aside 20% of your net income into a separate savings account, and then live on whatever is left.

60/40 budget plan

The 60-40 budget rule for money is another budgeting option that only assigns two categories to your spending plan:

- 60% for all necessary expenses

- 40% for everything else

Could it be any simpler? If you appreciate a less restrictive spending plan, the 60-40 budget plan might be the method you want to try.

In conclusion: find the best method for your budgeting goals

If you feel overwhelmed with all of the budgeting decisions that are necessary for your day-to-day money management, you may want to try a budgeting strategy based on percentages. These methods can make budgeting for household expenses, debt repayment, and savings goals easier to achieve.

There are many budgeting techniques you could apply to your personal finances. Whatever you do, don’t let any confusion you have about the concept of budgeting deter you from using one for your own finances.

Budgeting is the best way to reach your long-term savings goals, carry out your debt payoff plans, follow a college savings plan, and save for the retirement you dream about.

You can use pen and paper, a spreadsheet on your computer, or even a budgeting app to simplify your efforts.

For further budgeting advice, read my post on 33 budgeting tips for beginners. There are also many good budgeting books out there – check out your local library or Amazon.com.

The important thing is to use some type of budget tracker that helps you stay on track with your day-to-day budget and focused on your financial objectives. Choose one of the budgeting strategies outlined in this post, and start being more intentional with your money goals.

Other posts you may enjoy:

- 100 Money Journaling Prompts To Improve Your Financial Life

- How To Get Rich With A Normal Job In 2023

- Planning Your Dreams: 3 Simple Steps To Creating Your Dream Life

- Why Is It Important To Set Financial Goals? Here Are 9 Powerful Benefits

- 23 Smart Strategies To Save For Retirement At 50

- Pinecone Research: An Easy Way To Make Extra Money

- How To Beat Lifestyle Inflation In 8 Steps

- How To Make An Extra $1000 A Month: 50+ Profitable Side Gigs

- How To Save $1000 A Month (Without Working More)

- 50+ Fun Money Saving Challenges To Save More In 2023

- A 5-Step Plan To Save $5,000 In A Year

- 50 Smart Ways To Save Money On A Tight Budget

I hope you enjoyed reading