Table of Contents

Beginner tips for following a budget

If you’re tired of feeling out of control with your money, then I’m glad you’re here. Starting out as a beginner with budgeting might seem overwhelming, especially if your finances are in a mess. But, in this post, I’m going to tell you everything you need to know about budgeting so you can get on a spending plan that works for you. So, stick with me!

Starting and keeping a budget is one of the most effective ways to get control of your finances, align your spending with your values, and achieve your budgeting goals.

Don’t be too hard on yourself if you’ve been procrastinating with this important financial habit. Just follow the budgeting tips I’ve outlined below, and you’ll be well on your way to being the boss of your own money – even if you’re starting a budget from scratch.

Learning how to budget isn’t difficult, but following the right personal budgeting tips will help you be successful. Even if you’re a beginner, you’ll understand how to create a spending plan that tracks your expenses and maximizes your income.

Are you ready to learn how to set up a budget and stick to it? Great!

But first, let’s go over some budgeting basics.

What is the purpose of a monthly budget?

For some people, the word “budget” can leave a bad taste in their mouths. It’s synonymous with restrictive or confining, but this is just an unfortunate misconception of this powerful financial tool.

A simple definition of a personal budget is a spending plan that tracks your income and expenses, and guides your spending decisions over a specific period of time.

Said a different way, a budget is a plan you create in advance for managing your income. You’ll use some of your income for expenses, some for saving, and some for giving. Your budget will reflect how you want to allocate your sources of income across all three areas, without spending more than you earn.

How would budgeting help me?

There are many benefits to budgeting, as you’ll soon learn. But, the best way a budget can help you with your money management is by giving you a spending plan to follow.

Achieving your financial goals requires specific action steps, such as spending less and saving more. You can use your budget as a “guide” to help you stay on track and improve your financial health.

If you can stick to your budget, you’ll be able to cover all of your expenses, pay off your debt, and still add money to savings. You’ll also be more prepared to handle any unexpected expenses that pop up.

33 budgeting tips for beginners

Follow these simple, but powerful, budgeting tips to start mastering your finances.

1. Know your money values

Being clear about what you value when it comes to your personal finances will help you align your spending with your priorities.

Like most people, you probably value the goal of becoming financially independent and debt-free. If so, make sure your budget reflects this by prioritizing saving and debt payoff.

But, what else do you value when it comes to money? Having enough to take a nice vacation once a year with your family? Saving college funds for your kids’ education? Being able to retire on time, without fear of running out of money?

These are all values that should inform the goals you set and how you set up a realistic budget.

Make a list of money values, and use them as a guide for managing your money.

2. Have a savings goal in mind

As a budget beginner, it’s very important to know why you want a budget. This can be determined by setting a few goals, so you have something to work toward.

Creating some inspiring money goals will give you a target on the horizon, and your budget can help guide you toward it.

When setbacks arise (and they will), use your goals to give you the motivation to get back on track and moving forward.

Here are a few good reasons to have a budget:

- Pay off your credit card debt

- Start a down payment fund for a house

- Build up your retirement fund

- Be on the same page with your spouse

- Stop living paycheck to paycheck

Keeping your money goals in mind will influence the budget you create, and then help you stick to it.

3. Know how much monthly income you bring in

Budgeting helps you maximize your income, but first you need to know how much money you bring in every month.

Your income could come from a number of sources, such as:

- Paychecks from your regular job(s)

- Any extra paychecks from freelance work or side gigs

- Business income

- Investment income

- Alimony or child support

- Rental income

- Social security

- Unemployment

There may be some income sources that don’t pay out every single month. This is when it’s a good idea to create an “income calendar” so you can adjust the budget when your income varies.

Be sure to use your after-tax income for budgeting purposes. Account for all of the deductions taken out, such as federal and state taxes, social security, 401(k) and HSA contributions, etc. This will give you the actual income you’ll use to budget your monthly living expenses.

If your income fluctuates from month to month, try taking an average over the last 12 months and use this as a monthly “salary”. I’ve found the best way to budget variable paychecks is by budgeting with the previous month’s income … more on this later!

4. Start tracking your spending

If you haven’t been on a budget, you’ll probably need to do a little digging to find out how you’re spending your money now. This will give you a good starting point to create a budget that’s realistic and reflects your current financial situation.

You’ll also discover those areas where you’re overspending, and what budget cuts you can make.

Track your financial transactions for at least 30 days to get a good idea of your spending patterns. There are a few ways you can do this:

- Write every expense down, from your mortgage payment to that mocha latte. Track every dollar that’s coming out of your bank account. You can do this in a spreadsheet, a budget planner, or a checkbook register.

- Download an app like Mint or PocketGuard and link it to your bank account. Streamline the tracking process by assigning labels to various spending categories.

- Use your bank and credit card statements from the previous 30 days. This works especially well if you use your debit card and online bill pay for the majority of your spending (rather than getting cash from an ATM). Even if you don’t remember what some transactions were for, you’ll still have a general idea of how you’re spending your money.

5. Separate your fixed, variable, and periodic expenses

Your budget will consist of fixed, variable, and periodic expenses. It’s a good idea to know how they’re different, so you can manage them effectively.

Fixed expenses are those that recur on a regular basis, and don’t typically fluctuate a lot. Many times you’re under a legal contract to pay them, so it’s critical that they are a priority in your spending plan. Bills like your mortgage, auto loan, cell phone, and monthly bank fees are considered fixed expenses. However, unnecessary expenses like monthly subscription services are also fixed.

Variable expenses are expenses that can be either necessary or discretionary, and they also fluctuate from month to month. Some of these costs are easier to adjust and you can often find options that will reduce (or eliminate) their impact on your budget. Groceries, entertainment, clothes, personal care items, and hobby expenses are all considered variable expenses.

Periodic expenses (also known as irregular expenses) aren’t paid in every budget cycle. These occasional expenses may happen annually (like vehicle registration), every 6 months (auto insurance premiums), or whenever an occasion calls for one (like going to the vet or changing your tires).

In your tracking log, categorize each expense into one of these three. This will give you a general idea of what percentage of your income needs to be allocated to each type.

6. Decide on a budgeting method

To set up a budget, you need to know which type of budget works best for you. There are a variety of budget methods to choose from, but here are the most popular 3 options:

50/30/20 method

This personal budgeting method, created by Senator Elizabeth Warren, separates your money into 3 major expense categories – fixed, variable, and debt payoff/savings. It’s not a strict method, but it helps you fit your expenses or spending into each category so you can stick to your budget.

With this budget strategy, you spend 50% of your regular income on your fixed expenses, 30% on variable spending, and 20% on debt payoff and savings.

This method is very simple, flexible, and won’t get you tripped up on details. Just assign each expense to one of the 3 categories, then adjust your budget so each category stays within its percentage.

Cash-based budget (envelope method)

This method assigns an envelope to each category in your budget. You fill the envelope with the allotted amount of cash. Once you spend the money in the envelope, you’re done spending in that category for the month.

This cash-based budget works well to budget any remaining income after your fixed expenses have been paid. Having envelopes for budgeting categories like dining out, entertainment, or shopping will help you stick to your budget and not overspend.

If you don’t want to follow every dollar in your bank account, this may be an effective method for you. All you have to do is fill your envelopes with cash, and stop spending when the envelope is empty.

Zero-sum method

The zero-sum budget gives every dollar a ‘job.’ At the end of the month, you should have a $0 balance – not because you spent all your money, but because you were intentional with where every dollar went.

So, just as you have categories for housing, food, and entertainment, you also assign some of your income dollars to savings, investing, and giving.

This budget method requires more detailed tracking but is very effective for taking control of your finances and maximizing your income. You can read more about this strategy in my zero-sum budget guide.

7. Pick a money tool to create your spending plan

You can make your budget on paper, or create an online spreadsheet with Excel or Google Sheets. It all depends on what works best for you, and what you think you’ll stick to.

I have a Google Sheet spreadsheet with one main budget template, and then a separate tab for each month. I simply copy the template to the current month, and make any necessary adjustments for any irregular income or expenses.

Using a digital budget sheet allows you to use formulas that automatically update totals as you input new amounts in each category. As long as the formulas are correct, your numbers will always be accurate.

If you prefer to budget on paper, there are many free monthly budget worksheets you can find on the internet. Just be sure to always double check your totals with a calculator, so you don’t base future updates on incorrect numbers.

8. Choose and prioritize your categories

Your budget will be unique to your financial situation. Therefore, you should choose those budget categories that are relevant to you. You can be as general or specific as you like, but don’t have so many that updating your budget becomes complicated.

I like to keep general budget categories for most living expenses, but I also have a few specific ones that I like to keep track of.

Here are some ideas to get you started:

GENERAL | SPECIFIC |

Housing | Mortgage |

Food | Groceries |

Transportation | Gas |

Personal Care | Hair salon |

Medical | Doctor |

Fun | Entertainment |

Next, you need to prioritize your categories.

Your mortgage payment and utility bills must be paid so you have a place to live. Then, you need to have money for groceries and gas. Finally, you have to meet your debt payments.

After you cover your basic needs, you’ll need to determine what’s a priority to you. These expenses might seem like they’re necessary, but they’re actually not. Or, at least, their cost is not fixed.

These could include:

- Savings

- Insurance coverage

- Monthly subscriptions

- Personal care costs

- Charitable giving

- Entertainment

Decide what your money values are, and budget accordingly. Perhaps you’re spending a lot on new clothes, but you realize this is actually a low priority. Make the necessary changes in your budget so your spending plan is a reflection of what you value most.

9. Include a Miscellaneous category

No matter how well I plan, there always seem to be extra expenses that aren’t in the budget. I used to balance the budget by taking money meant for another category to cover these unplanned costs.

Now, I keep a “miscellaneous” budget category as a catch-all for these types of expenses. I only keep $100 in this category, because I don’t want to overspend on trivial purchases.

If there’s any left over at the end of the month, I just add it to our savings fund.

10. Get intentional with your food budget

One budget category that can quickly get out of control is food. The good news is, there are a few steps you can take to save money with your restaurant and grocery budget.

First, set a tight budget for eating out. Maybe commit to once a week, and know your spending limit each time.

Second, make more meals at home. Making your own food is a fraction of the cost of a restaurant bill.

Third, create a meal plan every single month. Write down 20-30 meals you’ll prepare at home, and create your grocery list from the recipes you pick.

A meal plan will keep you from buying groceries you don’t need, cut down on your grocery shopping, and keep you from making spontaneous trips through the drive-thru.

Once you’ve done these three steps, you’ll be surprised how much money you’ll save on food!

11. Make it a rule to give every dollar a job

If you want to maximize your income, then you need to account for every dollar you make. After you add up all of your income sources, be sure you have a place for every dollar to go.

This doesn’t mean you’re spending all of your money so you have nothing left at the end of the month. It just means that every dollar has a job – which could include going towards a bill, your monthly giving, or a savings account.

When you budget this way, there is no income that’s wasted or unaccounted for. This is sometimes called a zero-based budget, because all of the money coming in minus all of the money going out should equal zero.

12. Create sinking funds through your bank

Sinking funds are a great way to intentionally save for future expenses. Instead of having one general savings account, you dedicate separate accounts to specific saving goals.

For example, if you’re thinking of replacing your car within the next year, set up a “new vehicle” sinking fund. Add enough savings to this account every month so you’ll have enough to pay cash when you’re ready.

Here are a few other ideas for sinking funds:

- Annual expenses, like insurance premiums or car registration

- Christmas gifts

- Summer vacation

- An upcoming wedding

- College tuition

Determine how much savings you want to add to each sinking fund every month, and then create a budget category for each account.

Setting up a few different sinking funds will help you stay focused and on track with achieving your financial goals.

13. Save bills and receipts in one place

When your monthly bills and receipts are unorganized, budgeting can become frustrating real quick. Keeping them all in one place will make updating your budget easier and faster.

If you like to keep hard copies, you can put them all in one folder. Be sure you regularly empty your wallet of the receipts you collect, and let your partner know where to put them as well.

Personally, I try to stay digital as much as possible. I get all of my bills delivered to my email, which I put into one email folder called “Bills To Pay”. For paper receipts, I pin all of them to a bulletin board in my kitchen and update my budget every other day.

I only keep receipts that I may need for returning an item. All others I toss once I’ve updated my budget.

14. Keep a calendar of irregular expenses

It’s a good idea to write down a list of dates for non-monthly expenses. This way you can prepare ahead of time for upcoming costs that aren’t in your regular budget.

An easy way to do this is by using a calendar. Just use your online bank account or paper statements to review the last 12 months. Then, add to the calendar every expense that wasn’t made on a monthly basis, such as:

- Gifts for holidays, birthdays, showers, anniversaries, etc.

- Auto registrations

- Insurance premiums

- Property taxes

- Federal and state taxes

- Annual memberships or subscriptions

15. Create a savings category to pay yourself first

This was the #1 priority my parents taught me about managing finances. Always pay yourself first.

This simply means that you put money in savings *before* you pay bills, buy groceries, or spend money on the extras.

If you’re in your 50s, then you might be focused on increasing your retirement contributions. Setting up a direct deposit to a 401(k) or IRA is one way to pay yourself first.

Or perhaps you’re trying to build an emergency savings fund, or save money for a big purchase. Pay yourself first by creating a savings category in your budget that must be paid every month.

16. Have an emergency fund

If you don’t have any savings set aside for emergencies, this should be your first savings goal to work toward.

Without any emergency savings, you will likely have to rely on credit card debt to cover any emergency expense, like repairing your car or replacing that washing machine that decided to stop working.

These unplanned expenses will just add to your debt load and increase your credit card payments, not to mention the added interest you’ll have to pay.

Start setting aside a little money in a separate emergency fund that’s dedicated to financial emergencies that must be paid for quickly. This will greatly help you stick to your budget and stay on track with your goals.

17. Make retirement a priority

Take care of your future self by making your retirement savings a priority in your budget. Your money needs a long period of time to grow, so it can support you for the last 20-30 years of your life.

If your employer offers a 401(k), be sure you’re adding money to one from every regular paycheck. Also, always take advantage of any matching funds by meeting your employer’s percentage. This is free money in the bank!

Open an IRA as a second option, and set up a direct deposit to your account so your retirement savings is automatic.

Learn to live without this money now, so you’ll have it when you’re no longer working.

18. Pay off credit card debt as fast as you can

Yes, you need to pay bills and save money. And, while you’re doing that, pay off your debts as fast as possible.

How in the world?

It’s a balancing act, for sure. But the only way you can be successful is if you’re in control of your finances with a budget.

The faster you can pay off your high-interest credit cards, student loans, and medical bills, the more money you’ll save in interest and have to put toward savings. Come up with a debt payoff plan that’s aggressive, but reasonable. You’ll need to make more than the minimum payment on your balances to see progress quickly.

If your budget is tight and it seems like you’ll be in debt forever, it might be time to make some major adjustments. Here are a few things you can do to ramp up your debt payoff efforts:

- Get a second job

- Sell a vehicle

- Downsize your housing

- Rent out a room

- Start a side hustle

19. Keep some fun money in your household budget

Once you start your budget, you might be tempted to really crack down on your spending. However, if you don’t leave some room for having a little fun, you’ll quickly experience budget burnout.

Make sure you include a category that covers those things you enjoy doing. This might be going to the movies once a week, investing in your hobbies, or just going out with friends.

If your spending plan includes some fun money, you’re more likely to stick with your budget for the long run. (However, be sure you give yourself a reasonable limit so you still have enough to apply to savings and debt payoff!)

20. Know the difference between wants vs needs

As you learn how to budget in the beginning, you’ll become more aware of how you spend your money. You’ll realize that you spend a good amount of money on purchases that are neither necessary nor very beneficial.

Those things that you used to think you *must* have can start to fall lower on the priority list, because now you’re more focused on saving money or paying off debt.

This is a very helpful realization as your priorities shift and you become aware of the difference between what is really needed versus what you just want.

A helpful exercise is to write down 2 columns, with one side including all of the expenses that you truly need to live. This is basically shelter, transportation, food, and clothing.

The other side would be everything else – things that are nice to have, convenient, but not necessary.

You might be surprised how short the needs list is … and how long the other one can get.

Keep these lists handy, as a good reminder when you’re tempted to spend money on something you believe you really need. You might just realize you don’t.

21. Update your budget once a day

In the beginning, you should update your budget on a daily basis. I have found that even after a few days, my finances can get a little unruly if I don’t keep up with it.

Take a few minutes each evening to add that day’s transactions to your budget template. Add up how much you’ve spent so far in each category to see if you need to make any minor adjustments.

You don’t want to wait a week and realize your budget has gone completely off the rails. Be diligent with updating it every day so you maintain control and know exactly how much you have left in each category.

22. Review your budget once a month

Don’t expect to create the perfect budget at first. Most people need at least a couple of months to really find their budgeting groove, as they work out the kinks and make adjustments.

When you first start out, review your budget once a month to determine what changes need to be made. You might find that you need to add extra cash to some categories while reducing the budget in others. This is totally normal, and eventually, you’ll have a better grasp of how you should allocate your monthly income.

Your budget should be a stable but flexible tool that you use to serve your overall objectives. Make revisions as necessary to ensure it continues to help you make progress toward your goals.

During the first 3 or 4 months, you may make several major changes to your budget as you learn how to manage your money. After that, your budget template will probably only need a few occasional tweaks.

23. Keep your budget accessible

Budgeting for beginners can be a tough habit to build. It’s important to build momentum with daily updates and monthly reviews. You need to keep your spending plan front and center as you’re developing a budget mindset.

For this reason, keep your budget easily accessible. If you’re using a notebook, keep it somewhere visible, like the kitchen counter or your home office desk.

If you have a digital budget, with an online spreadsheet or mobile budget app, then you can access it from anywhere with a laptop or cell phone. This makes it easy for your spouse to access it as well.

24. Keep track of your progress

I have to admit, budgeting isn’t the most exciting way to spend my time. But, what really helps keep my motivation going is seeing how much closer I am to my goals.

It’s important to keep track of where you once were, where you are now, and the progress you’re making toward your own goals. So, when setbacks arise, you won’t just throw in the towel.

You can download a free savings tracker or make your own. Put it somewhere that’s visible so you’ll see it often. Create a vision board, and include all of the things you’re looking forward to. Make it a regular part of your day to be reminded of what you’re working toward.

If you’re married, encourage each other in what you’re accomplishing together. Talk about the future with great anticipation, and support one another as you both work toward your common goals.

25. Use cash to prevent overspending

You’ll probably discover that you often overspend in certain budget categories, like groceries or gifts or entertainment.

Stick to your budget by using cash just for these expenses. Put your budgeted amount in an envelope, and only use this cash when you spend on that particular category.

Cash in hand is harder to let go of than running your debit card through a machine. This means you’ll be more selective with what you spend your money on, and it will last longer.

Once the cash is gone, the spending stops. This is a great way to keep from going over budget!

26. Break the impulsive spending habit

As you begin to budget and track your spending, you might notice you spend a considerable amount on unplanned, unnecessary expenses. This is called impulsive spending, and it’s a bad financial habit that will quickly bust your budget with reckless expenses.

Once you become aware of how often you make impulsive purchases, you can take steps to break the habit.

Here are a few ideas:

- Always shop with a list, and never buy anything not on the list

- Commit to waiting 24 hours before making an unplanned purchase

- Avoid spending temptations, like subscriber emails or shopping when you’re emotional

- Use cash only, which will cause you to be more selective with your spending

You’ll find that breaking the impulsive spending habit will free up more money for other things you value more – such as making extra payments on your mortgage.

27. Automate your finances with bill pay and direct deposit

This beginner budgeting tip will set you up for greater success in your finances. By automating your monthly payments and savings, you make your money management easier.

The fewer choices you have to make when it comes to your finances, the better.

Set up your online bill payments through your bank’s website so you never miss another due date. Then, automate transfers into a separate account so your savings is not an option. You can do this through your online bank account, or set up split direct deposits through your employer.

Automate your finances so the work is done for you, and you can focus on how to spend less and save more.

28. Use budgeting apps for added support

There are several popular budgeting apps out there that will help you with your budgeting. Most of them connect to your bank accounts and will categorize your transactions for you. A mobile app will also break down by percentage where your money is going.

These mobile apps are great resources that can help you stay on track, but I don’t recommend using them exclusively as you begin to budget. Checking in with a mobile app is a passive way to manage your money, and taking control with a budget requires more hands-on input.

Here are a few popular budgeting apps:

- Mint

- PocketGuard

- You Need A Budget

- EveryDollar

- Goodbudget

Check with your bank as well. They might have a very effective budgeting app that you would prefer to others.

29. Have a plan for extra money

Receiving some unexpected money is always a nice surprise, but this extra income can quickly disappear without a plan in place.

Decide ahead of time how you will handle these extra funds. Perhaps you’ll want to put 50% in savings and 50% towards debt. Or you’ll always apply 75% to your mortgage and 25% to your vacation fund.

From gifted money to a big tax return, these are great opportunities to get to your goals faster. Whatever you decide, having a plan for extra money will ensure that it serves a purpose when it falls in your lap.

30. Budget with last month’s paychecks

This is my best tip for beginner budgeters with variable incomes.

For many years, my husband worked an hourly position with varying amounts of overtime. His paycheck was different practically every week! I really struggled with budgeting his income, until I discovered this strategy.

Basically, you’ll need to determine a fixed amount that will cover all of your monthly expenses. For example, you might decide that $6,000 will cover all of your expenses every month.

Then, over several months, you save up this amount. Perhaps you can set aside $1,000 a month, which means you’ll reach your goal in six months. Once you have your monthly budget amount saved, you can start using this method.

First, you’ll transfer this amount from savings to your checking account and use this money for all of your expenses. You’ll also transfer all of the income you receive in the month into a separate savings account. So, as you’re using your savings for your monthly budget, you’re also replenishing your savings with income as it comes in.

So, every month, you actually use the income you made in the previous month to budget for the current month.

I love this method, because I don’t have to be concerned about how much each check is going to be. I know exactly how much money I have to use for the budget, and I have it all on the first of the month. This means I can pay all of my bills right away, do the bulk of my grocery shopping, and cover any other known expenses before I start spending on other things.

31. Have regular meetings with your spouse

Setting up a budget isn’t meant to be a chore that’s delegated to one spouse. Sit down with your partner and work on your budget together with regular money meetings.

Your spending plan and financial goals need to include both of your inputs. This way, you’re on the same page and working together as a team as you manage your combined income.

Decide on regular budget meetings together, and make sure each of you gives some input into your monthly money decisions.

32. Have an accountability system in place

Being held accountable is an important step in budgeting for beginners because, without it, it’s easy to lose momentum and let things slide.

Setting up accountability could look like any of the following:

- If you’re married, set up weekly, bi-weekly, or monthly ‘money dates’ with your spouse. Use this time to go over your budget and talk about where you’re succeeding and where you may need more help.

- If you’re single, set up reminders on your calendar to revisit your budget periodically to see how you’re doing. If you notice areas you’re overspending or aren’t sticking to your budget, take the time to figure out what you can change.

- Meet with a financial coach if you can’t stay on track. If you find it impossible to stick to a budget, consider meeting with a financial advisor. Look for someone who helps with spending, financial goals, and helping you align the two so you can make progress.

- Automate whenever you can. Set up payments through your bank’s online bill-pay feature, create automated transfers into savings on a regular basis, and have contributions directly deposited into your retirement account. This will reduce the number of financial decisions you have to make and help you stay on track with your financial goals.

33. Expect setbacks, and give yourself time

When you start budgeting, you might feel a lot of hope that you’re finally going to get control of your finances. This is true – but you need to be aware of a few things so you don’t get discouraged.

First, as a budget beginner, you’ll need to give yourself a bit of time to work out the kinks. You’ll probably go over budget in a few categories, and wonder how you’ll ever save up for that new car. You’ll definitely encounter a few setbacks that make you feel like you’re going backwards.

This is all normal. It can take a while to get the hang of budgeting.

Whatever you do – don’t stop budgeting.

The kinks will smooth out, you’ll overcome those setbacks, and you *will* find that money for a new vehicle. Budgeting is an ongoing process, and it just takes time to master.

If you go into the budget process knowing that there will be bumps along the way, you’ll be prepared to persevere toward your financial goals. Don’t give up!

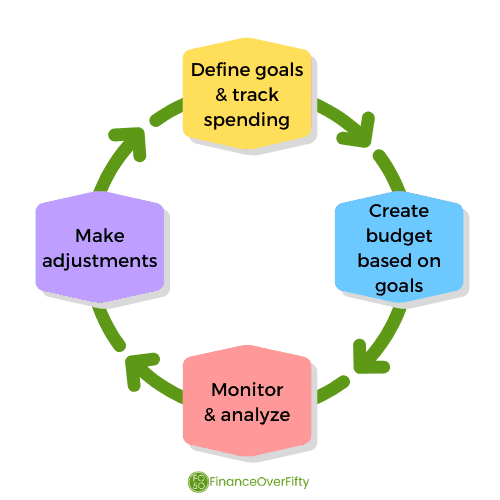

How do I start budgeting?

There are several ways you could start budgeting your money because it all depends on your own circumstances and preferences. However, if you want your budget to be an effective tool that supports your goals, there is a common process across any method you choose.

Just as a budget has a cycle (like weekly or monthly), the budget process can also be described as a loop that perpetually repeats, getting you closer to your goals:

- define financial goals

- track spending and understand spending patterns

- create a budget based on goals and realistic expectations

- monitor your budget and analyze for effectiveness

- make adjustments as necessary to align your spending with your values

The budget process is meant to coordinate your financial circumstances with the goals you want to achieve. In this way, you can use your budget as a tool that helps you map out a financial strategy.

Following the budgeting process will increase your awareness of destructive financial decisions and spending patterns that are hindering your progress. You’ll discover what changes need to be made with your lifestyle and your mindset if you want to be successful with your finances.

Of course, we call them “personal finances” because they’re personal. How you choose to budget and carry out the process will be unique to your financial situation.

Your budgeting process will be based on a few factors:

- which budget method you use

- how you track your spending

- how you categorize your expenses

- how often you update your budget

- what budgeting tools you use

- what your money values are

Making these decisions ahead of time will help the budgeting process go smoother for you.

How to choose categories and percentages

Having appropriate budget categories will keep your spending plan organized and easier to analyze. However, it’s easy to get stuck on which ones to choose and how many to have.

The good news is, there is no right or wrong way to pick your budget categories. You can get as general or specific as you like. Simply create your categories based on the spending patterns identified in your tracking.

The important thing is to have a category for every single expense. Whether you have 3 or 33, just make sure you can fit every transaction into one of them.

Here is one example of a budget category list:

- Income

- Housing

- Insurance

- Utilities

- Automotive

- Debt payments

- Entertainment

- Clothing & Shoes

- Groceries

- Dining Out

- Household Items

- Personal Care

- Savings

- Charitable Contributions

When it comes to percentages, you can go super simple with the 50/30/20 budget method. If you need more structure, you can use Dave Ramsey’s suggestion to limit your mortgage or rent to 25% of your net monthly income and keep all other categories between 5-15%.

Here is an example of budget percentages you can refer to:

- Housing: 25%

- Insurance (including health, medical, auto, and life): 10%

- Food: 10%

- Transportation: 10%

- Utilities: 10%

- Savings: 10%

- Entertainment (anything fun): 10%

- Clothing: 5%

- Miscellaneous: 10%

Avoid these common budgeting mistakes

Although budgeting your money isn’t difficult, it does take time figure out what works for you. You will inevitably hit some snags along the way that could potentially throw you off track.

Be prepared by knowing the common budgeting mistakes most people make. This way, you can either completely avoid them yourself, or at least minimize their impact on your efforts.

Here are just a few common budgeting mistakes to be aware of:

- Basing your budget on expectations that are unrealistic

- Creating a budget with your pre-tax income

- Failing to plan for irregular expenses

- Not having an emergency fund

- Continuing to use debt to cover expenses

- Using estimations instead of exact numbers

- Being unwilling to make lifestyle changes

All of these common budgeting mistakes will cause you to go over your budget. If you handle each one early in your budgeting journey, the process will be easier and you’ll experience greater success.

Digital budget planners to help you stay on track

If you work best with a pencil, paper budget, and a simple calculator, then feel free to stick with those tools. But, there are many more resources available that can make budgeting easier, faster, and more efficient.

I’ve mentioned a few tools already, and I’ll also include them here along with a few others that are helpful with budgeting:

- Mint

- PocketGuard

- ClearCheckbook

- Excel or Google Sheets for spreadsheets

- You Need A Budget (YNAB)

- EveryDollar (by Dave Ramsey)

- Goodbudget

- Quicken

Some of these can track your spending automatically, which can be really convenient. However, I don’t recommend relying on an app to do this when you’re just starting to budget. Taking a hands-on approach in every aspect of your finances will help you stay tuned in to what your money is doing. Once you have a good handle on sticking with a spending plan, you can hand over the tracking to a digital tool.

FAQs

How should a beginner start a budget?

To be successful with budgeting, there are a few steps you can take to get started:

1. Set a few financial goals that are specific and time-bound

2. Track your spending to know your spending patterns

3. Create a budget with categories that reflect your values

4. Update and review your budget often to stay on track

5. Make any adjustments that help make your budget better align with your goals

When should I start budgeting?

The sooner you can create and start a budget, the faster you’ll gain control of your household finances and start saving more money. Don’t overanalyze the process – just pick a method to track your spending and start. You will learn from your mistakes and make changes along the way.

How much should I save out of each paycheck?

How much you decide to save each month will depend on your financial goals, and the amount of disposable income you have. If you cut expenses and increase your income, you can free up more money to save and reach your goals faster.

What are the best apps for budgeting?

There are several good mobile apps to help you with your budgeting. Mint, Pocketguard, EveryDollar, and GoodBudget are just some of the many apps available. Try one out for 30 days, and if it doesn’t work for you, then try a different one.

Which budget method is best for me?

The budget method you choose will largely depend on how closely you want to track your money. If you don’t want to get too specific, then try the 50/30/20 budget method. If you want more control over every dollar, I recommend the zero-based budgeting method.

Don’t overanalyze this decision! Just pick a method and give it a go. Try it out for a month or two, and feel free to switch strategies if it’s not working for you.

As long as you keep a balanced budget (where income equals expenses), you won’t be living beyond your means.

How do I stick to a budget?

A good rule of thumb to help you stick to your budget is to use cash instead of a card. Handing over money instead of swiping a card gives you a better idea of how much you’re actually spending and keeps you from going into debt.

What happens if I go over my budget?

You wouldn’t be the first person to have a bad month and spend more than you budgeted. The important thing is to not make that a reason to stop. Take a deep breath, pick up where you are, and keep going! Just like any other habit, sometimes you’ll get off track. The important thing is to try again.

What is the bare-bones budget method?

A bare-bones budget is a type of basic budget that only accounts for necessary expenses. You would use a bare-bones budget in times of dire financial circumstances, or if you want to cut out all unnecessary costs to reach a financial goal. If you’ve lost your job, using a bare-bones budget method will help you maximize your emergency fund.

How do I stay motivated to keep budgeting?

People often get discouraged when they first start budgeting. For many, it’s the first time they’ve come face to face with the true state of their finances – and it can look pretty bleak.

This is when your financial goals become your motivation to persevere past the feelings and focus on your future. If you want to stay committed to your budget, it’s important to identify those financial goals that your budget will help you achieve.

Without goals that align with your budget, then you’re merely tracking your money without making progress toward financial freedom.

In conclusion: use these budgeting tips for beginners to crush your budget goals

If you’re ready to admit you need to start a budget, you’ve taken the most important first step. Congratulations!!

Budgeting for beginners isn’t as hard as it seems, and I hope this post has given you some helpful guidance for putting a budget into action.

Creating a budget is the beginning of a journey toward financial control. Your financial goals are the destination you want to eventually reach. In between, there will be many distractions, temptations, and barriers that can keep you from making progress.

You will probably encounter many points along the path where you go off course. There will be times when you’ll want to stop moving forward and even go backward. You may even decide to take a detour or a different route.

Don’t let these delays keep you from trying again. The only reason you’ll fail is if you give up!

It’s never too late to start fresh and make better decisions with your money. The sooner you start with these simple budgeting tips for beginners, the more in control you’ll feel and the faster you’ll meet your financial goals.

Other posts you may enjoy:

- Why Is Saving Money Important? Here Are 50 Inspiring Reasons!

- 39 Essential Sinking Fund Categories For Your Budget

- 17 Powerful Benefits of a Budget

- 50 Ways To Stretch Your Food Budget

- The Cheapest Way To Live: Best Tips For 2023

- Money Values: How To Align Your Priorities With Your Spending

- 50 Ways To Save Money On A Tight Budget

- 9 Powerful Benefits of Setting Financial Goals

- 51 Fun Money Saving Challenges To Save More Money In 2023

- How To Resolve Money Issues In Marriage

- The Essential Retirement Roadmap For Late Starters

- Financially Sound: What It Means and How To Get There

Want to save this post for later? Pin it to your favorite Pinterest board!