Table of Contents

Why it’s important to set financial goals

Have you ever wondered, why is it important to set financial goals? If so, then I’m glad you’re here.

In this post, I’m going to share with you the many proven benefits of setting financial goals. Learn how you can experience amazing positive changes in your life by getting specific with what you want and taking intentional action.

Just having big dreams or good intentions isn’t enough. If you want to fully realize your vision for your financial life, you need to map out a plan that will make that happen. This includes setting goals that support your values and priorities.

Having meaningful goals can set you on a path to a debt-free life, and guide your journey to financial freedom.

The benefits of setting financial goals all work together to boost your financial health. You’ll gain more confidence in your money management decisions and significantly decrease money-related stress.

If you want to take control of your money and create a more financially secure life, you need to set some financial goals.

Ready to crush your financial goals? Get this FREE financial goal tracker today!

What are the benefits of setting financial goals?

Establishing financial goals is a critical step toward success, stability, and security.

When you decide how you’re going to manage your money in order to achieve the life you want, you begin to align your actions with your goals. This is how you set your life in motion toward a specific outcome.

Life goals, in general, benefit your life by creating focus, motivation, and confidence. But, when you include defined financial objectives in your life plan, you set yourself up for successful outcomes that benefit several areas of your life.

Here are 9 benefits of setting financial goals:

- You can create an effective action plan for your finances

- You can choose appropriate strategies

- You can measure your progress

- You know what your priorities are

- You strengthen your motivation and commitment

- You increase your chances of experiencing positive outcomes

- You create built-in accountability

- You improve your money mindset

- You have hope and confidence in your future

All of these benefits create powerful change in your life, and they will inspire you to make financial decisions that move you closer to your larger goals.

Let’s go over each one in detail.

#1 Financial goals guide your planning

Once you’ve decided on specific financial objectives, you can design an overall plan to achieve them. When you know where you want to end up, you just have to fill in the steps to get there.

These steps are just “pieces” of your bigger goals. For example, let’s say you have a long-term goal to be debt-free in 5 years. You would break down this big goal into smaller targets along the way. These might include cutting expenses, increasing your income, and doubling your monthly payments.

These smaller goals act as milestones on the way to fulfilling your long-term vision. They inform you how much you need to save to reach your big goal. Some will be reached sooner than others, but they all contribute to achieving your big objective.

These milestones guide your financial planning, and reaching every target helps push you forward to the next one.

And, as you categorize your goals into short, mid, and long-term, they collectively create a timeline for you to follow. This allows you to create an effective and realistic plan to reach your big goal.

#2 Financial goals inform your strategies

When you plan a road trip, you typically begin with your destination. Then, you decide what route you want to take to get there.

Your personal ambitions can be achieved in many different ways. But, depending on your timeline and circumstances, the path you take to reach them will vary. Different financial objectives will require different strategies.

When you’ve set your financial goals, you have a high-level view of where you’re going. This perspective will help you determine the tools and methods that would best support your efforts in reaching them.

You might choose a certain budgeting process or investment vehicle because it offers the greatest potential progress within the time frame you’ve set. Or, you might choose between the debt snowball and debt avalanche methods to wipe out your debt balances.

The only way to make a choice with confidence is by having clearly defined goals that inform your strategies.

Then, you can implement the most efficient means of achieving them successfully.

#3 Financial goals provide measurable progress

Setting financial objectives provides a way to measure your progress so you know if you’re on the right track or not.

As you take the necessary actions to achieve your goals, the results you experience can give you perspective and insight. They allow you to identify what’s working, and what needs to be adjusted.

Having a standard to measure yourself against creates the awareness to self-evaluate and self-correct when necessary. Knowing when and what to change in your financial plan is critical to achieving your goals on time.

Also, seeing how far you’ve come and how much closer you are to your goals is a great way to boost motivation.

#4 Financial goals help you focus on your priorities

If you’re never clear about what you want to achieve in life, you’ll lack direction. And, if you don’t have direction, then you’ll lack focus. This leads to distractions that ultimately pull you farther away from what’s really important to you.

Setting financial objectives will help you focus on your priorities, so you’ll begin to align your actions with your values. They act as a filter that eliminates those tempting distractions.

This may lead you to make some tough decisions, like no longer helping your adult children with expenses or fully funding their college education.

When your current decisions are based on your long-term vision, it’s easier to make choices that support your objectives. You’ll have more confidence in how you manage your money because you know your actions reflect your priorities.

Also, being focused on what’s important means you’re less tempted to spend extra money on stuff that doesn’t contribute to your overall progress. You’ll be more committed to making financial decisions that move you closer to your achievable goals.

#5 Financial goals strengthen motivation & commitment

Being specific about your financial objectives not only gives you direction, it also creates the motivation to persevere through adversity. As you move closer to your target, your commitment to reach it gets stronger.

Many people avoid setting goals because they fear the disappointment of failure. However, failure is often a necessary stepping stone to success and offers valuable lessons.

As you come against setbacks and unexpected difficulties, your goals provide the motivation to keep moving forward.

When you set specific goals, you also create clarity about your future. If you have a clear idea of where you’re heading, and what’s possible for your life, you’ll more likely follow through with taking action.

Related Post: How To Motivate Yourself To Achieve Your Goals

#6 Financial goals improve your chances of success

As mentioned before, setting financial goals provides the clarity needed to create the positive results you want in your life. If you don’t define the outcomes you want to experience, your journey toward financial freedom will be cloudy at best.

Someone smart once said a dream without a plan is just a wish. In other words, if you’re only dreaming about what could be, and never taking action, you leave it to circumstances to determine if your dream will ever come true.

Setting defined financial objectives propels you into actionable behavior and your chances of actually realizing your dreams greatly increase. Once you’ve charted your course to achieve them, you set yourself in motion toward a successful outcome.

#7 Financial goals provide built-in accountability

For some people, the road to a financially secure retirement is paved with good intentions. That’s because many fail to move from just good ideas to a specific, well-written plan.

And, if there is no plan, there is nothing to be accountable for.

Accountability is important when it comes to goal setting because it establishes responsibility. Your goals are like benchmarks you set for yourself, and it’s ultimately up to you to reach them. This creates a sense of ownership that contributes to a successful outcome.

Writing down your financial objectives and reading them every day is a powerful habit to practice. Daily reminding yourself of the improvements you want to make in your life will instill a deep sense of responsibility for making progress.

#8 Financial goals will improve your money mindset

You can practice all the best money habits, but you’ll never achieve financial freedom if you have an unhealthy money mindset.

Your money mindset is your own beliefs and attitudes about money. These beliefs drive your behavior, which leads to results.

So, if you believe that you’ll never get out of debt, or that you’ll never make more money, or that you’ll never have enough to retire … guess what?

You probably won’t.

The beliefs you have about money shape the way you manage your money. In other words, your actions will inevitably confirm your beliefs.

Setting financial objectives can help you create a healthier money mindset. The productive habits you develop and the progress you experience foster a more positive outlook that breaks those old beliefs over time.

As you experience small successes along the way, you’ll have a sense of achievement. This will allow you to open yourself up to greater possibilities.

You start believing in yourself and in your ability to create a better future. You become more comfortable with risk, and you’re more willing to explore new directions. Your mind opens up to a big-picture view, and you begin to see all of the amazing opportunities around you.

That’s when your mindset shifts and your beliefs inspire actions that lead to positive and prosperous results.

Related Post: 4 Disguised Fears Holding You Back From Achieving Your Goals

#9 Financial goals can foster hope and confidence

Have you ever been driven around by someone who doesn’t know where they’re going? Maybe your spouse took you to an appointment and insisted they could find the building and get you there on time. But, after five u-turns, you began to lose faith in their navigational skills.

Having a map to guide you is one way to feel confident that you’ll get to your destination. You know the address and you have the directions to get there. It’s just a matter of following the map.

Setting financial objectives is like creating a map for your money management. Once you determine where you want to end up, your goals act like landmarks along the way. With each one you reach, you know you’re going in the right direction and you’re closer to your destination.

You’re confident and hopeful that your journey will be a success, as long as you keep moving forward.

Having defined goals takes the guesswork out of your financial planning. You know the steps you need to take, and you’re confident that your actions are supporting your personal ambitions.

And, when you’re confident in your decisions, you have hope they’ll lead to a better life.

Now that you know the powerful benefits of setting financial goals, you might be wondering about the best way to make your own.

Of course, this active process can be as simple as creating a list of objectives that are meaningful to you. But, the more specific you are with your goals, the greater chance you’ll have of following through and making them a reality.

Later, I’ll go over 5 steps to set financial goals and stay committed to your plan. But first, let me give you a few examples of the three types of financial goals.

What is a financial goal?

Financial goals are the specific intentions you decide for your money. Your goals are unique to your personal financial circumstances, and they give you defined targets to aim for. They represent the ideal outcome of your financial decisions over time.

Financial goals should be specific, measurable, achievable, and time-based.

Your goals also need to be meaningful, relevant and aligned with your values.

You’ll also want to organize your goals into categories of time. Creating short-term, mid-term, and long-term goals will help you stay on track with your financial targets.

Examples of financial goals

There are three main types of financial goals: short-term, mid-term, and long-term. Whether you want to get out of credit card debt or save for a dream vacation, any financial goal can be categorized as one of these three types.

The more specific you can make your goals, the better chance you’ll have of achieving them. Setting a goal date and identifying a measurable result will help you stay focused and on track.

Here are some examples of each type of financial goal.

Short-term financial goals examples

Short-term financial goals can be set for anywhere from one day to 2 years in the future. They are the objectives you can achieve within a relatively short amount of time.

Your short-term goals should always get you closer to your medium and long-term goals. They are the “quick wins” in your overall financial plan.

Here are some examples of short-term financial goals:

- Pay off $5,000 of credit card debt within 18 months using the debt avalanche method

- Save $1,500 for a summer vacation before May 1st

- Purchase life and disability insurance within 12 months

- Open a tax-advantaged retirement account like a 401(k) or IRA within 3 months

- Start meal planning this month to cut food expenses by 25%

- Shop around for lower auto insurance premiums this week

Medium-term financial goals examples

Medium-term goals for your finances (also called “midterm”) should be achievable within 2 to 5 years. They take longer to reach than short-term goals, and they’re like the bridge between your short-term and long-term objectives.

Here are a few examples of mid-term financial goals:

- bring your credit score above 800 within 2 years

- Increase monthly retirement saving contributions to 15% within 3 years

- pay off my $10,000 personal loan within 4 years

- save $20,000 for a European dream vacation in 3 years

- have a $40,000 down payment for a new home within 5 years

- build a 6-month emergency fund within 2 years

Long-term financial goals examples

Your financial planning should start with your long-term goals, which can take anywhere from 5 to 20 years to achieve. That way, you can break them down into medium-term and short-term goals.

They are your biggest objectives, so they typically require the greatest time and financial commitment.

Here is a short list of long-term financial goals:

- build $50,000 in additional savings for college tuition within 10 years

- be free of student loan debt within 15 years

- pay off the mortgage within 20 years

- fully fund my retirement accounts by the time I’m of retirement age

- generate $10,000 a month in passive income by my 55th birthday

Now, let’s go over how to create your own financial goals.

5 steps to set financial goals you’ll stick with

If you’re going to take the time to set goals, you’ll want to make sure you choose ones you’ll actually commit to. Take these 5 steps to create money goals that inspire you to take action:

1. Be specific

Thinking “I’d like to save more money” is an idea.

But, writing down I’m going to put $500 into my savings account every month for a year is a goal.

Get specific with details and action items. Know exactly what you want to accomplish. A goal needs to be clear and concise.

2. Make them measurable goals

If you can’t measure your progress, your goal isn’t specific enough.

You must be able to quantify results so you can break down your overall goal into smaller pieces that can be measured. This way, you can create actionable steps that inevitably move you forward.

Don’t leave room for interpretation or opinion. Have clear and defined milestones that serve as evidence of progress, so you can stay focused and motivated.

3. Give them a time frame

A big mistake many people make when setting goals is not setting a deadline. As a result, their goal keeps getting pushed back because less important, every day tasks take precedence.

According to Parkinson’s Law, “work expands to fill the period of time available for its completion.” If you give yourself an endless amount of time to achieve a goal, you will continue to fill up your hours with busy work and never see it fulfilled.

Giving yourself an end-date will boost motivation and sharpen your focus. You’ll be able to prioritize more effectively when you are bound by a specific amount of time.

4. Know your why

Just like you need to get specific about your goals, you also need to be crystal clear about the reasons behind them.

If you don’t have an emotional connection strong enough to drive your actions, you’ll give up at the first sign of adversity.

The goals you set for yourself likely came from a desire to improve your life in some way. You believe they’ll benefit you and contribute to a better future. This sounds good, but it’s not enough to carry you through setbacks and disappointments.

Ask yourself why a goal is important to you. How will it affect your life? What impact will it have on your family and loved ones? What would happen if you don’t achieve it?

Keep digging until you find the core reason that creates a strong emotional connection to the goal. This will typically be related to what you value most in life, like your family, your faith, or your purpose.

Knowing your why will be the strongest motivating factor throughout your journey to achieve your goal. Take the time to get real about your reasons.

5. Put your goals in writing

Studies have shown that people who write down their goals experience a greater success rate in achieving them. Why is this?

Putting your goals in writing forces you to get clear and focused. It’s the start of taking action. It’s putting yourself in motion.

You also create a visual cue that reminds you where you’re headed. When you take a bit of time to review your written goals, you motivate your actions. You become more intentional about aligning your behavior with your priorities.

Written goals also turn daydreams into declarations. They’re no longer passive thoughts, but they become something tangible that you can see, read, and interact with. This small switch is a powerful force that tells the brain to start seeking solutions that will help you achieve your goals.

Don’t keep your goals in your head. Put them down on paper, and review them every day.

Video: How To Set SMART Goals

Habits that help you achieve your financial goals

If you want to achieve your goals, you’ll need to develop smart habits that keep you on track.

Money habits are like the stepping stones that get you from the starting line to the finishing line. They’re the behavior systems that support the results you’re trying to achieve.

Good habits take time to develop. But, once they become second nature, you can rely on them to get you where you want to go.

Here are a few smart money habits that can help you achieve your financial goals:

- Track your spending and follow a monthly budget

- Make purchases with cash, and minimize debt

- Avoid lifestyle inflation and live below your means

- Automate your savings contributions with bank transfers and direct deposit

- Make savings a priority and always pay yourself first

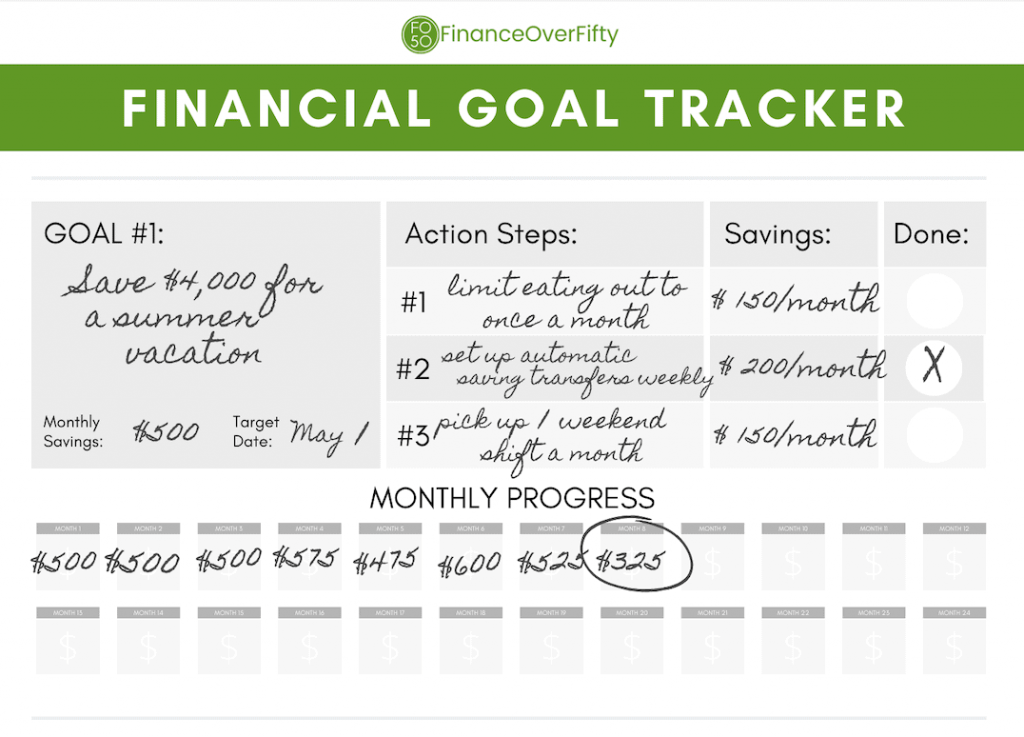

How to track your progress with a financial goal chart

Set yourself up for success by creating a chart that tracks your progress toward your financial goals.

A financial goal chart will help you get specific with a timeline, strategies, and actionable tasks.

Here are six concrete steps you can take to create your own financial goal chart:

- Write down one financial goal that you want to achieve.

- Determine the financial commitment the goal requires.

- Decide an end date for when you could realistically achieve this goal.

- Break down that financial commitment into monthly saving goals.

- Write down effective action steps you can take.

- Track your monthly progress.

Let me show you an example:

You can make your own financial goal chart and tracker, or download a free one from this page!

Keep your options open and adjust when necessary

Nobody knows what the future holds, so it’s important to maintain a degree of flexibility when it comes to your financial goals. Life rarely goes as planned, so know what your options are and adjust your course when you need to.

Losing the job you’ve held for 20 years, or getting diagnosed with a debilitating disease, can throw your plans off track overnight.

Prepare for these setbacks before they happen. Have a backup plan you can implement, so you can minimize any negative repercussions.

You might need to reprioritize or shift your goals, so they fit better into your new circumstances.

For example, if your retirement plans revolved around retiring early, you could extend your timeline a few more years. Or, if your goal was to pay for your kids’ college tuition, you may have to split the bill or pick a less expensive college.

The point is, having a financial plan – regardless of life’s curveballs – will prevent your dreams from falling off the rails when life takes a sudden turn.

You may even choose to meet with a financial professional, who can offer tremendous support in helping you reach your financial goals.

Here are just a few ways a financial advisor can help you:

- meet with you regularly to evaluate your progress

- determine if adjustments need to be made

- give you relevant financial advice

- offer investing assistance with retirement funds

- guide your efforts with saving for retirement

Don’t forget to grab this FREE financial goal tracker today, and start crushing your goals!

In summary: It’s important to set financial goals for yourself

I believe everyone is born with a sense of purpose, but most of us lose it as we get older. It gets buried under the challenges of life, and we lose sight of the bigger picture. So many people settle for what life gives them, instead of being intentional about creating a life that reflects their purpose.

One of the main benefits of setting goals is to line up your purpose with your actions. They give you direction, focus your energy, and give you a sense of accomplishment when achieved. They help you to be future-oriented.

And “purpose” doesn’t have to be a huge deal. It’s not always about your life’s purpose. It could be a smaller purpose that helps you get to the larger one.

Goals are born out of a vision – typically, one that will improve the quality of your life. If you don’t have a vision for your future, and one you can connect your biggest goals to, you will end up settling for whatever life hands you.

It’s important to have goals that will guide your actions and provide motivation to keep going. To keep moving forward toward a richer, more fulfilling life.

Don’t let circumstances determine your results. Don’t be passive with your awesome retirement dreams.

Get future-focused. Take control. Start changing the course of your life.

You have a big part in creating a better future for yourself, so set some financial goals and start making it happen!

Other posts you may enjoy:

- 100 Money Journaling Prompts To Improve Your Financial Life

- How To Make An Extra $1000 A Month: 50+ Profitable Side Gigs

- The One Thing Summary: How Going Small Leads To Big Results

- How To Get Rich With A Normal Job In 2023

- Why Is Saving Money Important? Here Are 50 Inspiring Reasons!

- How To Take The 100 Envelope Challenge & Save $5,050

- How To Save $1000 A Month (Without Working More)

- 5 Principles To Change Your Life After 50

- What Does The Bible Say About Debt? 50+ Verses For Financial Freedom

- 5 Ways Limiting Beliefs Harm Us

- 4 Disguised Fears Holding You Back From Achieving Your Goals

- How To Meet Your Future Self and Change Your Life

- A Willingness To Change: Here’s the How & the Why

Want to save this post for later? Pin it to your favorite Pinterest board!

I hope you enjoyed reading