Table of Contents

What you need to know about Dave Ramsey sinking funds

Dave Ramsey is a financial guru who has created many products to help people get out of debt and save money. One way he helps you do this is by implementing sinking funds.

In this blog post we will be discussing why Dave Ramsey recommends sinking funds, what these funds are, how they work, and how you can use them for your own financial situation.

Watch your savings grow with this FREE sinking funds tracker! Download today and start saving for your dreams!

What is a sinking fund?

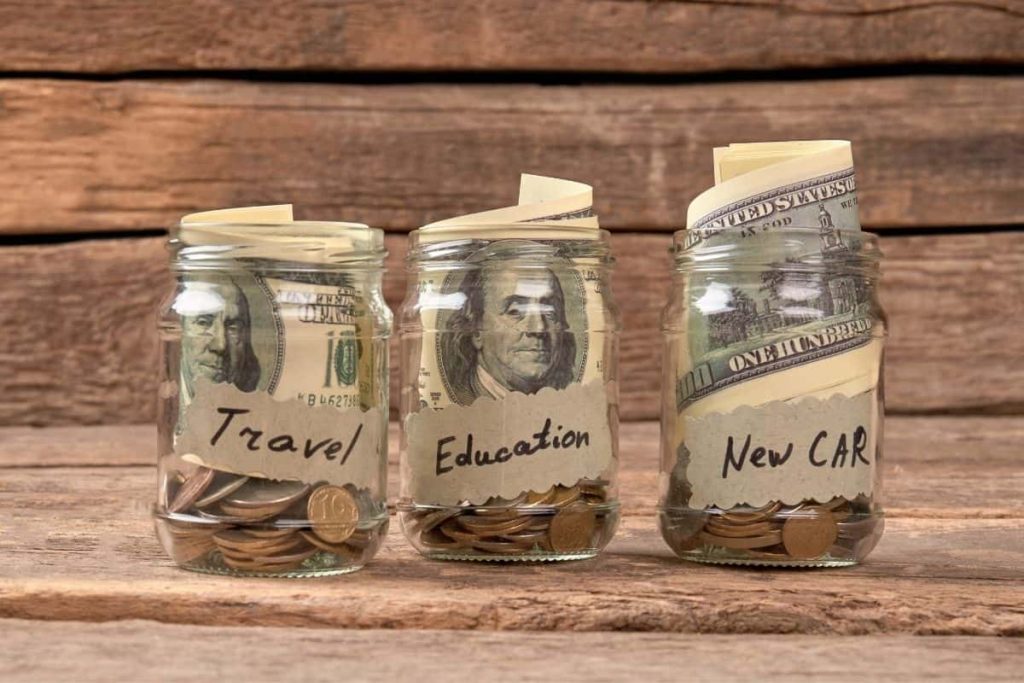

A sinking fund is a saving strategy that is used to make future purchases by saving small amounts over a set period of time.

You can use sinking fund money to pay for planned expenses, such as vehicle registration fees, a new washing machine, or even a dream vacation. You choose those annual expenses that you want to save for systematically, based on your financial obligations, values and goals.

A sinking fund may sound a lot like an emergency fund or a savings account, but they aren’t exactly the same. Let’s go over the differences between both.

Sinking fund vs Savings account

While a savings account is typically used as a place to set money aside for general purposes, a sinking fund is assigned as a specific budget item in your monthly spending plan.

Another difference between these two accounts is that a sinking fund usually has a predictable expense attached to it. Once you reach this savings goal in the sinking fund, you don’t need to keep adding to it.

A sinking fund allows you to be more intentional and focused on specific savings goals. Because each sinking fund has one specific purpose, you can easily see how close you are to reaching specific financial goals.

Sinking fund vs Emergency fund

Maybe more important that saving for the expected, is having savings set aside for the unexpected. This is what an emergency fund is for.

An emergency savings account is typically one fund to collect all savings for any unexpected expense in the future that must be paid for immediately. So, while a sinking fund is for some future, expected purchase, the emergency account is used for the unknown.

For example, you could use your emergency fund savings if you suddenly get a flat tire and have to replace it with a new one right away. But, you would use a sinking fund to save up for new tires because you know (eventually) the ones you have are going to wear out.

Why does Dave Ramsey recommend sinking funds?

Like any wise financial educator, Dave Ramsey strongly encourages his students to follow a few fundamental principles: follow a budget, be aggressive with debt payoff, and save money. Each of these takes adequate time, intention, and patience, but they all lead to financial freedom.

When it comes to sinking funds, Dave Ramsey knows how this simple method can help you reach your goals and financial freedom as well. With some strategic saving, you can avoid being stuck in debt and be more intentional with your money.

How do I create a sinking fund?

If you think you want to include sinking funds in your financial plan, you may be wondering what is the best way to create them.

The most common way is with separate savings accounts, but you can also use other methods such as envelopes, or even have just one big sinking fund and keep your fund categories organized with a spreadsheet. Whichever method you choose, the process is basically the same.

Here’s how to create a sinking fund in 5 steps.

Step 1: Decide where you want to keep your sinking funds

As I just mentioned, this might be several separate savings accounts, in envelopes, or one dedicated sinking fund for everything.

Make sure the method you choose makes it easy for you to save. With savings accounts, you can set up automatic deposits for every payday and not have to think about it. With envelopes, you’ll need to be more disciplined with adding cash to each one. If you choose to have one large sinking fund, it will be important to keep it organized and updated.

Step 2: Determine your savings strategy

Write down your current savings strategy and schedule for each fund so you know how much is going where and when. Then, keep this schedule somewhere visible so you’re often reminded of your saving goals.

If you set up automatic transfers, this won’t be as necessary because the saving is being done for you.

Step 3: Include your sinking funds in your monthly budget

Think of them as regular expenses that you have to pay in your normal budget. Treat them like any other bill in your monthly budget worksheet, and pay them first. Don’t wait until the end of the month to see what’s left over!

Set your financial goals at the top of your budget in terms of priority.

Step 4: Track your progress and adjust when necessary

Depending on what each sinking fund is for, you’ll achieve your savings goals at different times. It will probably take you longer to fully fund a sinking fund for a new car than a new dishwasher.

Keep track of the progress for each fund so you now how close you are to each savings goal. You can do this with a digital spreadsheet or just pencil and paper. Once you’ve saved enough in a fund to pay for that expense, take that savings payment and apply it to a new or different fund.

It’s important to be disciplined but also flexible with your savings goals. Make adjustments as you see fit, because priorities can change. You may decide you no longer want a new car fund, but instead a car repair fund for your current vehicle. Or perhaps a kitchen remodel has to be put on the backburner so you can save more for getting a new coat of paint on your house.

Step 5: Stay focused and diligent

Saving money is a habit that doesn’t come easily for most people. You’ll need to exercise a little discipline and patience to stay on track.

Keeping a tracker for your progress and having an accountability partner are two ways you can stay committed to your savings goals.

How many sinking funds should I have?

By now, you might be thinking that you should set up a sinking fund for every major purchase or expense you expect to make!

However, the more you have, the less progress you’ll make in each one. If you have 20 sinking funds but can only save $200 a month, that’s only $10 in each one if you distribute your savings evenly. It will be years before you can pay for that new widescreen in cash!

This is why you should carefully consider what your financial goals are, and how you’re going to prioritize them.

If you still have a lot of debt (aside from your mortgage), it’s a good idea to pay that off before you start your sinking funds. You also should have at least a starter emergency fund set up as well. Remember, sinking funds are for things you will need or want to buy sometime in the future. You want to be debt-free and prepared for emergencies now!

With that said, first write down a list of every category you think a sinking fund would be helpful for. Your list will probably be too long, but that’s okay. You’ll narrow it down later.

Next, consider how much total savings you can apply to your sinking funds every month. If you’re not sure, look at your budget to calculate the difference between your necessary expenses and total monthly budget income. Anything unnecessary could be potentially applied to your sinking funds.

If you don’t have a budget, start one! Track your spending and record every transaction so you can see how and where you’re spending every dollar. This is the best way to learn how you can maximize your income and save more money.

If you discover that you only have an extra $200 to save, you may want to have fewer sinking funds than if you had $1,000 for savings. It just depends on how quickly you want to reach your financial goals.

Once you know how much you can save every month, narrow down your list to the categories that are most important to you.

Let me give you a couple of examples. Here’s the first one, if you have $200 to save each month:

- Auto maintenance (oil changes, new tires, etc) $50

- Birthdays $25

- New washing machine $75

- Family vacation $50

And here’s the second example if you have an extra $1,000 to save monthly:

- New vehicle $200

- Gifts (birthdays, weddings, holidays) $100

- Vacations $300

- Annual premiums $100

- Taxes $50

- Home improvement $100

- College fund $150

Your list will reflect your financial priorities, so take the time to figure out what’s important to you and your partner.

(And, because it bears repeating, pay off any lingering debt and have emergency savings set aside first!)

How do I use my sinking funds for payment?

As explained previously, sinking funds are used to save money for future expected purchases. So, the first way to use them is by systematically and consistently funding each one with a set dollar amount at certain times over a predetermined period.

Sinking funds are for saving, but they’re also for spending! Once you’ve reached your balance goal and you’re ready to make your purchase, simply transfer that money to your regular checking account. Don’t do this step until you’re going to spend it though – otherwise, those savings might get eaten up by other, less important things.

How much should I save each month in my sinking funds?

An easy way to determine how much you should save in a sinking fund is by setting a deadline to reach your savings goal.

For example, let’s say you want to replace your current vehicle with a newer one within 2 years. Decide how much you’re willing to spend, then divide that amount by 24 months. This will be how much to put in your New Vehicle Sinking Fund every month for the next 2 years.

Or, perhaps you decide in January that you don’t want to charge any Christmas gifts that year. You set your gift budget category at $600 and create a sinking fund. You would then need to save $50 in your Christmas Gift Sinking Fund every month to reach your goal.

Obviously, how much you save depends on what you can fit into your budget. However, there are ways to increase your savings capacity. Let’s go over a few.

How to save more money in your sinking funds

If you’re already living paycheck to paycheck, you might be thinking there’s no point in creating sinking funds if you have no money to put into them.

But, if you’re willing to adjust your money mindset and get serious about money management, there are ways to widen the gap between your income and your expenses. The wider the gap, the more you can save.

First and foremost, get on a budget. This is the first step in taking control of your finances. When you know where every dollar is going, you can find those miscellaneous spending leaks that are preventing you from reaching your financial goals. Consider cancelling subscriptions you don’t use, minimizing eating out, or finding lower insurance premiums.

Second, if you don’t have any goals – set some! Have a specific direction you’re moving towards. Get intentional with your money. Be purposeful with every dollar so you maximize the income you’re already making.

Third, increase that income. This is where the money mindset comes in. It’s critical to believe that you can increase your income any time you want to. When your mind is open to making more money, your eyes will open to the opportunities all around you.

Here are just a few ideas:

- get a part time job on the weekends

- ask for a raise

- apply for a promotion

- find a better-paying job

- have a yard sale or sell your unused items on NextDoor or Craigslist

- take on a side-gig such as driving for Uber, delivering groceries, tutoring high school kids, etc

- start your own business like consulting, web design, housecleaning, pet sitting, or catering – just pick what you’re good at, skilled at, or enjoy doing!

Once you start generating extra income, funnel all those extra dollars into your sinking funds so you can reach your goals faster.

Common sinking fund category ideas

I listed a few sinking fund ideas previously, but here is a more extensive list to give you more ideas:

- Home improvements

- Auto maintenance

- Auto replacement

- Insurance premiums

- Gifts (birthdays, wedding, holidays)

- Holiday & Birthday party expenses

- Wardrobe spending money

- Vet bills

- Dream vacation

- School expenses

- New appliances/electronics

- New furniture

- Landscaping

- Medical expenses

- Taxes

- Annual membership dues

- Educational activities

- School tuition

- Charitable giving

- A wedding or other special event

- Personal care expenses

- Personal business expenses

- Irregular expenses

- Annual expenses

How to maintain and track your sinking funds

It’s important to pick a tracking method for your sinking funds that will make it easy for you to see your progress.

This will depend a lot on your preferences. You might prefer pencil and paper over a digital tracker, or a simple list over a detailed spreadsheet.

It doesn’t really matter how you choose to track your sinking funds, as long as you’re consistent. If you prefer a manual approach, be sure to use a calculator so your numbers are accurate.

Some like something more visual, like filling in an image of a savings jar. Or you could create a form you complete once a month. Pick something you look forward to updating and is easy to maintain.

Once you’ve chosen your tracking method, decide how often you’ll update it. You might decide every payday, or the beginning of every budget cycle, or the last day of each month. Then, set a calendar reminder so you don’t forget!

Common mistakes to avoid with sinking funds

As simple as it can be to set up sinking funds, there are things you can do that will make it more difficult to achieve your goals. Here are 4 common mistakes to avoid when you’re setting up your sinking funds.

Not staying organized with your sinking funds strategy

One common mistake when setting up sinking funds is not dedicating those funds to a separate account. If you try to use your regular checking account to save money, you’ll find it more difficult to stay organized. It’s also easier to access those savings for impulse purchases you didn’t plan for. Always create a separate account for your sinking fund, or at least keep your savings somewhere besides your regular checking account (like in envelopes).

Having too many sinking fund accounts

Another mistake is setting up too many sinking funds. The more you have, the more you need to maintain, and the slower your progress will be. Consider having just one fund for gifts, instead of separate ones for birthdays, weddings, graduations, and holidays. You can create one sinking fund for educational expenses instead of having individual accounts for activities, supplies, fees and tuition. Choose your top 10 priorities, and focus on those first. Once a sinking fund is fully funded, you can create another one.

Not paying off debt first

A third mistake people can make is building multiple sinking funds while they’re still in excessive debt or before they have an emergency fund established. Consider using Dave Ramsey’s Debt Snowball or Avalanche method to pay off your credit card balances. Make sure your finances are stable and secure first, then set up your sinking funds.

Not keeping savings in a high-yield bank account

Finally, a fourth mistake that’s often made is not keeping your savings in a high-yield savings account. If you’re going to set up your sinking funds with bank accounts (as opposed to envelopes), you might as well make a little money off of them. Find a high-yield account where you can keep your savings until you’re ready to spend those funds. Opening a money market account is also a good choice. Just make sure you meet the minimum balance requirements so you’re not paying any monthly fees.

The benefits of using Dave Ramsey’s sinking fund method in your personal finances

One of the greatest benefits of sinking funds is that they allow you to stay out of debt. When you’re intentional with your savings strategies and consistently working toward achieving your financial goals, you set yourself up to avoid going into debt. Not only are you able to pay in cash, you’re paying the least amount because there’s no interest.

A second great benefit of sinking funds is how they support good financial habits. Saving money over an extended period of time strengthens your ability to delay gratification, avoid impulse purchases, and be more mindful about what you’re buying.

A third benefit is having more financial peace of mind. When you’re in control of your finances, you experience less stress over money and have fewer budget disasters. Being strategic and intentional will reduce worry, anxiety, and fear of your financial future.

One more benefit of using sinking funds is the increase in financial confidence you experience when you’ve achieved a financial goal. Being able to save money so you’re prepared for the future strengthens your belief in yourself to manage your money wisely. And – no guilt when you buy that new big screen!

How to include sinking funds in your budgeting plan

If you want to be consistent with adding extra cash to your sinking fund accounts, the best way is to include them in your budget. Make each sinking fund an actual “bill” that you pay by including each one as a line item in your budget.

Then, pay them first. Make it just as much a priority as your mortgage and electricity bill. Don’t wait until the end of the month to see what’s left over. Pay yourself first!

I use our last month’s income to pay the current month’s bills, so I pay everything (including savings) on the first of the month. This makes it easy to stick to our monthly budget goals and ensure we meet our savings goals every single month.

However, you might budget weekly, bi-weekly, or by paycheck. This means you might contribute to your sinking fund accounts more than once a month, depending on your income frequency.

No matter what your budgeting cycle is, the important thing is to be consistent with how much you’ll contribute to each sinking fund, and how often.

If you need help with setting up a budgeting routine, check out my post on how to use the zero-based budget method.

Don’t forget to grab your FREE sinking funds tracker! Watch your money grow and crush your financial goals!

Final thoughts on Dave Ramsey sinking funds

Knowing what sinking funds are and how to use them can help you work with your personal finances more effectively. They’re an effective strategic tool to help you save for your future and stay out of debt. They can provide stability and security, and allow you to reach your financial goals.

You may be wondering why it’s important, or think that this is just for people who need expert advice. That couldn’t be further from the truth! Take some time to read through these tips on understanding sinking funds so you know when they might make sense in your own life.

Start being intentional with your money. Be strategic with your savings. Create a few sinking fund accounts of your own and watch how easy it is to pay cash for even the largest purchases!

FAQs

Does Dave Ramsey recommend sinking funds?

Dave Ramsey, a well-known personal finance expert, recommends sinking funds to avoid using debt for upcoming expenses. Instead of using credit cards to pay for an amazing vacation, monthly birthday gifts, or holiday spending, he recommends being intentional with saving money before these expenses are due.

Should I have a sinking fund for retirement savings?

You could consider retirement accounts like a 401(k) or an IRA as a sinking fund for your retirement. These are much better options for retirement savings than a high-yield savings account.

How should I organize and keep track of my sinking funds?

You can organize your sinking fund monthly savings by setting up separate accounts for each one. Another idea is to use cash envelopes to organize your savings. Make sure you give each a label that indicates what it’s for.

You can keep track of these sinking funds accounts through savings goal trackers, or popular apps like Mint or You Need A Budget. Once you connect your accounts to the app, you can see all of them in one place.

Where can I find a sinking fund tracker?

If you like to write things down and follow your progress, you can use a sinking fund tracker. Download the free printable sinking fund tracker offered on this page, or do a Google search to find several sinking fund trackers to choose from. This is a great resource to track your savings toward each sinking fund expense.

What is the sinking fund formula?

This simple sinking fund formula allows you to determine how much you need to save every month to achieve a savings goal.

Total savings goal ÷ # of months to save = Monthly sinking fund deposit

Why is it called a sinking fund?

The term “sinking fund” has been used since the 18th century, to describe a dedicated fund for paying down national debt. In essence, the monies in the fund were used to “sink” the debt until it was paid off.

Although the sinking fund meaning used today (for personal purposes) is for avoiding debt altogether, this term is still used to describe money set aside for a future purchase.

What if there’s not enough in my sinking fund to cover an expense?

Sometimes you may discover that your savings goal did not cover the expense. However, a benefit of having multiple sinking funds is that you can take from one to add to another.

Perhaps your life insurance premium has gone up for the next year, and you’re $100 short in your sinking fund. You could borrow this amount from one or a few of the other funds, as long as those funds don’t need to be spent anytime soon. Just be sure to replace what you’ve borrowed!

What do I do with a sinking fund after I’ve used the money?

You will have some sinking funds for one-time expenses, and others for ongoing or irregular expenses. For those that are only needed for a single purchase, you have a couple of options after the money is spent. You can choose to close the account permanently, or use it for a new sinking fund.

Depending on what chapter of life you’re in, you will inevitably close sinking funds that become irrelevant. For expenses that are ongoing, you should replace the funds you’ve used until you reach the savings limit you’ve set.

Other posts you may be interested in:

- The Cheapest Way To Live: Best Tips For 2023

- 15 Scriptures On Debt Freedom: How To Handle Debt God’s Way

- Financially Sound: What It Means and How To Get There

- The Purpose Of A Budget: 17 Powerful Benefits

- How To Live On Last Month’s Income (and Why You Should)

- 14 (Mostly Free) Online Money Management Tools

- How To Live Within Your Means (and Still Be Content)

- Financial Health Checkup: 7 Steps To Boost Your Fiscal Well-being

- How To Escape Debt With A DIY Debt Management Plan

- The Zero-Sum Budget Resource Guide

- The Essential Roadmap For Retirement

- How To Create Personal Budget Categories The Smart Way