Table of Contents

What is Dave Ramsey’s Baby Step 3 all about?

Dave Ramsey created Financial Peace University as a 9-week personal finance program based on his bestselling book, Total Money Makeover. The program is designed to help people get on a budget, pay off debt, and create an effective financial plan that will lead to financial independence .

Here are the 7 baby steps in the program:

- Baby Step 1: Save $1000 in a starter emergency fund

- Baby Step 2: Pay off debt using the Debt Snowball method

- Baby Step 3: Build 3-6 months of expenses in a fully-funded emergency savings account

- Baby Step 4: Invest 15% of your household income into mutual funds for retirement

- Baby Step 5: Start a college savings plan for tax-favored college funds

- Baby Step 6: Pay off your mortgage

- Baby Step 7: Build wealth and give more

A fully-funded emergency fund is meant to protect you from life’s major curveballs – like losing your job, needing a long-term medical leave, or having your vehicle die on you.

Saving this much extra cash takes time, but can potentially save you from falling into a financial crisis or major debt.

In this post, I’m going to do a deep dive into Baby Step 3. This step is all about saving enough money to cover 3 to 6 months of your expenses.

Baby Step 3: What is an emergency fund and why do I need one?

An emergency fund is a cash resource that is allocated specifically for unexpected expenses that need to be addressed immediately. These unexpected events could include expensive medical bills, costly home appliance repairs, or a sudden job loss.

The beginner emergency fund from Baby Step 1 will help you get through small unplanned expenses, but you’ll need more cash reserves for those bigger curveballs life can throw at you.

Having substantial savings (like a three to six-month emergency fund) will minimize the dependence on high-interest debt during a real emergency.

This dedicated savings account also strengthens financial security, gives you peace of mind, and reduces the risk of falling into a financial crisis.

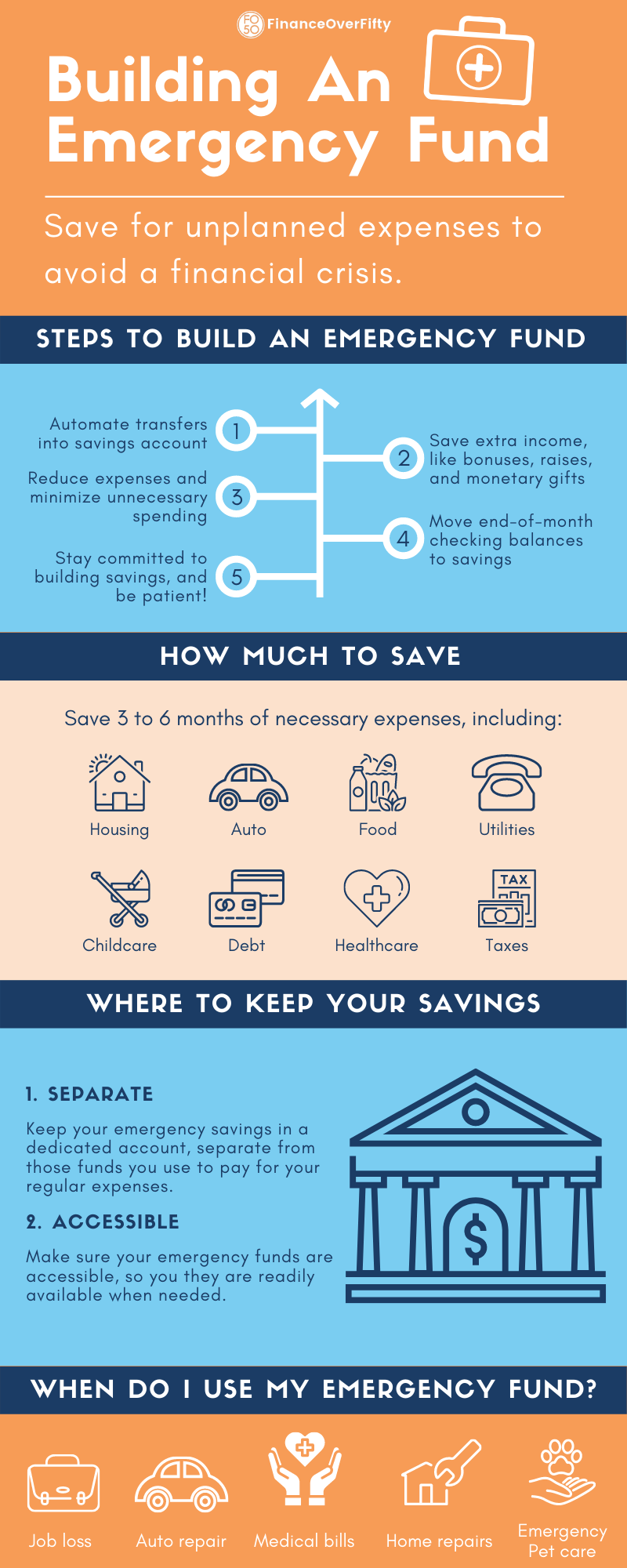

How much money should I save in my emergency fund?

The popular rule of thumb is to save 3 to 6 months of living expenses in your emergency fund.

Your savings target will depend on a few things, such as:

- how stable your regular income is

- how long you’ve been employed at the same company

- how many dependents you support

- if you have only one breadwinner or a two-income household

- if you’re self-employed or rely mainly on commission

- if you have high, recurring medical expenses

The more uncertain your financial situation is, the more you’ll need to save in your emergency fund.

If you are self-employed, a contract worker, or are the sole provider for your family, you should work towards the six month mark.

If you’ve had a steady full-time job for several years, or your spouse contributes a significant amount to your monthly income, you can stay closer to a 3-month fund.

And, remember that you aren’t working towards replacing your entire monthly income. Your initial goal is to have enough to cover all of your necessary expenses.

So don’t just look at your paycheck when figuring out how much you need to save. Look through your budget and pick out the categories that are non-negotiable.

These would be expenses such as your mortgage, utilities, and groceries. Leave off movie tickets and Starbucks frappuccinos.

Should I start an emergency fund when I still have debt?

You should only start Baby Step 3 once Baby Step 2 is completed.

As a quick summary, Baby Step 2 is about creating a debt payoff method to eliminate all of your debt except the mortgage (includes credit cards, student loan debt, consumer debt, credit card debts, etc.). Dave Ramsey recommends using the Debt Snowball method as the best approach to debt problems. This is where you pay the most on your first smallest single debt, while making minimum payments on the rest. Then, you focus on your second-smallest debt, and continue on until all that’s left is your largest balance.

Once you’ve achieved this huge accomplishment, the next step in the Financial Peace University course is to build a fully funded emergency fund.

The spenders who suffered through the discipline required to pay off debt may want to slow down at this point. But it’s critical that you keep moving forward with the same gazelle intensity as you move into Baby Step 3.

Because, in order to not slide backward, you must have a nice cushion of savings that will protect you when emergencies arise.

Yes, you can celebrate when you can finally say “I’m debt free!” – but don’t stop there. If you do, then Murphy’s Law will kick in, which means you’ll be charging that next emergency and be right back in a cycle of debt. Let the fear of that possibility motivate you!

Commit to never going back! Keep moving forward and start saving with the same intensity you had with crushing your debt.

Where should I keep my emergency fund?

Your emergency fund will grow to a sizable amount once you’ve reached your savings goal. Therefore, you should keep your money in a high-yield savings vehicle (such as a money market fund) so it can benefit from a higher rate of return. The best annual returns typically hover around 2%, and online banks often have higher rates.

Also, read the fine print about bank fees so you’re not losing money. You may need to maintain a minimum balance so you don’t get charged every month.

You want to make sure your savings stay secure and liquid. You do not want to be investing your emergency fund! Consider this savings a type of insurance rather than an investment. You always want to have cash ready at your disposal when emergencies arise. You can always talk to someone at your bank to get professional investment advice.

How do I save cash for an emergency fund?

The best way to find extra money to save comes down to 3 steps:

- Manage cash flow: Know where your money is going

- Decrease cash spending: Find monthly expenses to cut out

- Increase cash reserves: Make savings a priority in your budget

First, you must know how you’re currently spending your disposable income. This means tracking your money so you know where every dollar is going.

Second, find those areas where you can cut back, or eliminate altogether. Look for any extra cash that you can use to build your emergency fund. For some inspiration, read my post about how to save an extra $1000 a month without working more.

Third, create a budget and make savings a non-negotiable expense (read my post all about Dave Ramsey’s zero-based budget). Use a spreadsheet, or find a budgeting app that helps you stay accountable. Then, treat your monthly savings goal like it’s any other bill, and pay yourself first.

Depending on your current income level, monthly debt payments, and household expenses, saving a bunch of money for a 3 to 6-month emergency fund can take months, or even years.

My financial advice to you is to not focus on *when* you will get there. Instead, just stay committed to building your emergency account, one month at a time.

Finally, two important points:

- Talk to your spouse or partner about how you will define an emergency expense (e.g., a flat tire is an emergency, upgrading your phone is not).

- When you use all or part of your emergency fund, build it back up to its original balance. This needs to be priority #1!

What’s next

Of course, the amount of time it takes to complete each of these baby steps will vary for each person or couple.

For some, it could take years to pay off your biggest credit card debt. For others, the emergency fund may take the most time.

As your bank account changes, so will you. Your mindset, your behavior and your priorities will all start lining up with your one big goal: financial freedom.

You’ll also start to experience an amazing sense of security, and no longer dread an unstable future.

It takes time, focus, and sacrifice. You’ll be tempted to quit and go back to your old, comfortable habits. You might feel like everyone around you is moving forward with life while yours is standing still.

Remember what Dave says – live like no one else, so later you can live like no one else.

Baby steps 4-7 are next, and are meant to be done simultaneously. Once you’ve accomplished the Dave Ramsey Baby Step 3, continue to follow this step-by-step plan to become completely debt-free and achieve financial freedom:

- Dave Ramsey Baby Step 4: Invest 15% of your income into a retirement fund

- Dave Ramsey Baby Step 5: Start a college savings fund for your kids’ college education

- Dave Ramsey Baby Step 6: Pay off the mortgage

- Dave Ramsey Baby Step 7: Build wealth and give

They are all about looking towards your future. It’s where you work on building your income for retirement and accomplishing those dreams for your golden years.

Stop looking around you at what others are doing. Decide for yourself that you are committed to doing what it takes to reach financial freedom.

Keep going! You can do it!

Other posts you may enjoy:

- How To Build A 6-Month Emergency Fund In 5 Simple Steps

- 15 Smart Strategies To Save Money When You’re Broke

- How To Make An Emergency Fund Last Through A Crisis

- The One Thing Book Review: Going Small Leads To Big Results

- 8 Steps To Beat Lifestyle Inflation

- 5 Tips To Make Saving Money Easier

- 50 Smart Money Habits To Save More Money

- How To Get Rich With A Normal Job In 2023

- 50 Ways To Save Money On A Tight Budget

- 9 Powerful Benefits of Setting Financial Goals

I hope you enjoyed reading