Table of Contents

Liquid net worth is different than overall net worth

I’ve written before on the importance of tracking your net worth, which is a snapshot of your financial progress at a single point in time.

Basically, you calculate your net worth by subtracting what you owe from what you own. It’s a valuable metric to help you determine what financial levers you need to move in order to be ready for retirement on time.

But, there is another type of net worth, called liquid net worth, and is perhaps a more useful tool to gauge your financial health. Tracking your liquid net worth will allow you to know how close you are to financial security and financial freedom.

Although the net worth of the rich and famous is often discussed in the gossip columns, liquid net worth is a separate measurement that’s rarely discussed. Maybe because this calculation is usually much lower and not nearly as impressive.

To give you an example, Bill Gates is one of the richest men in the world and worth about $130 billion today in terms of net worth. But, this isn’t actually a good indication that he can go out and *spend* $130 billion on whatever he wants. Although his overall net worth is $130 billion, his liquid net worth is only a fraction of this because of his investments in real estate, art, antiques, and other non-liquid assets.

So, while your overall net worth is a reflection of your financial wealth, your liquid net wealth is a good indication of your financial health.

So, what exactly is liquid net worth? Let’s go over that next.

Get this FREE Monthly Metric Tracker to start tracking 4 important personal finance metrics!

What is liquid net worth?

As a subset of your total net worth, your liquid net worth only accounts for all assets that can be turned into cash quickly and efficiently.

To know your liquid net worth, you need to determine the value of your liquid assets (assets that can easily and quickly be turned into cash) and subtract your liabilities from this number.

This important metric indicates an individual’s financial security and health because it addresses the ability to generate cash relatively quickly in times of necessity and emergency.

So, even though you include your home, vehicles, real estate, and retirement accounts in your overall net worth, these can’t be converted into cash quickly and are therefore not generally included in your liquid net worth calculation.

What is a liquid asset?

Often, people will qualify a liquid asset as one that can readily be converted into cash within 24 to 72 hours. In other words, any asset that you can sell on a whim and receive cash in return should be included in your liquid net worth.

These could include:

- Cash

- Checking and savings accounts

- Mutual funds

- Personal checks

- Stocks

- Bonds

- Certificates of Deposit

Something to keep in mind is that there are no exact rules to determine what is a liquid asset and what is not. It’s up to you to determine which of your assets you consider “liquid” enough to include in the calculation.

For example, your home is not typically considered a liquid asset. However, if you live in a thriving real estate market where you know you could sell your home very quickly, you may want to include it with your other liquid assets. Just remember to discount its value for realtor fees and any applicable taxes.

Obviously liquid net worth is somewhat “fluid” in nature, meaning its calculation can depend on your circumstances and preferences. So, decide for yourself what purpose you want this metric to serve as a reflection of your overall financial security. If you want to calculate how easy it would be to liquidate assets within 24 hours, then you should restrict your assets appropriately. However, if you just want an idea of how much cash you could raise within 30 days, then your calculation would probably look different.

What is a non-liquid asset?

Any asset that can’t be converted to cash quickly is considered non-liquid and shouldn’t be included in your liquid net worth. Since it takes time to sell fixed assets like vehicles and properties, they are usually not considered liquid.

Non-liquid assets typically include:

- Real estate & property

- Vehicles

- Ownership in a business

- Artwork, antiques, and collectibles

- Retirement accounts

However, as mentioned in the previous section, it’s entirely up to you which assets you include in your liquid net worth calculation.

Just keep in mind that any asset besides cash may need to be discounted in value due to the costs necessary for a cash conversion. For example, if you want to include your 401(k) in your liquid net worth, be sure to discount its value by any early withdrawal penalty fees and taxes you would have to pay.

Your overall net worth will consist of both liquid and non-liquid assets. If you want more flexibility in your finances, increase the value of your liquid assets.

How to calculate your liquid net worth

Here is a straightforward formula to calculate your liquid net worth:

Liquid Net Worth = Liquid Assets – Liabilities

First, make a list of your total assets (liquid and non-liquid), which might include:

- Cash / Bank accounts

- Vehicles

- Real estate

- Retirement accounts

- Mutual funds, bonds, stocks, etc.

- Collectibles, art, jewelry, etc.

- Savings

Then, write down all of your liabilities, such as:

- Credit card debt

- Total remaining balance on your mortgage

- Car loans

- Student loans

- Payday loans, personal loans, and any other kind of loan

- Any other types of debt

Now, let’s go over an example of how to calculate both your overall net worth and your liquid net worth, just so we can compare the two.

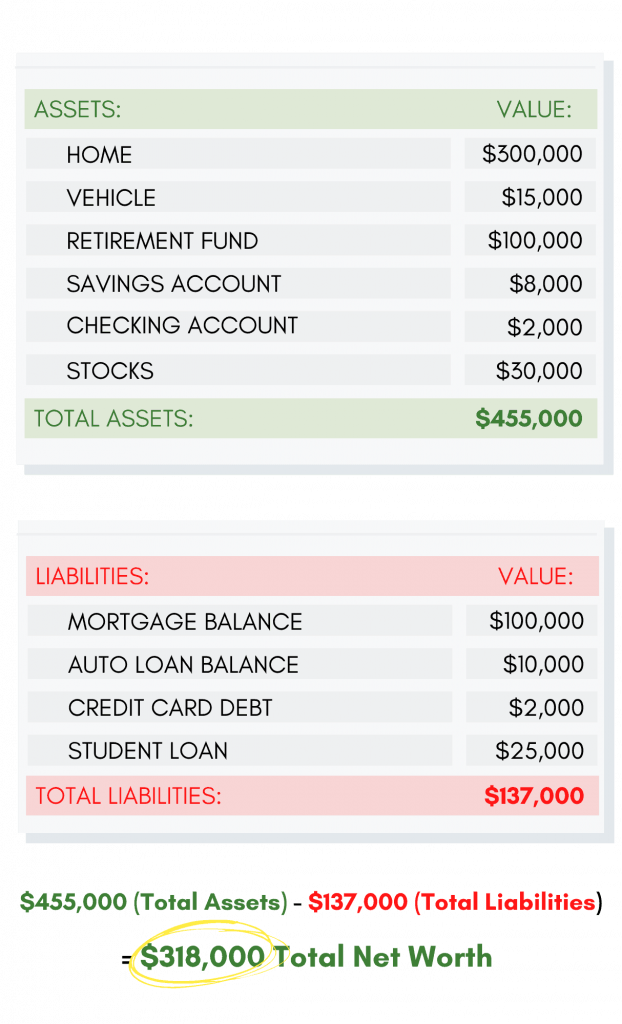

Perhaps your financial situation looks something like this:

- A house with a market value of $300,000

- A car valued at $15,000

- $100,000 left on a mortgage

- $10,000 left on a car loan

- Credit card debt of $2,000

- Student loan debt of $25,000

- $100,000 in a 401(k) retirement account

- $8,000 in your savings account

- $2,000 in your checking account

- $30,000 in stocks

To calculate your total net worth, you’d add your assets in their entirety and subtract your total liabilities. It would look like this based on the values listed above:

Pretty impressive, eh? Now let’s compare that to liquid net worth.

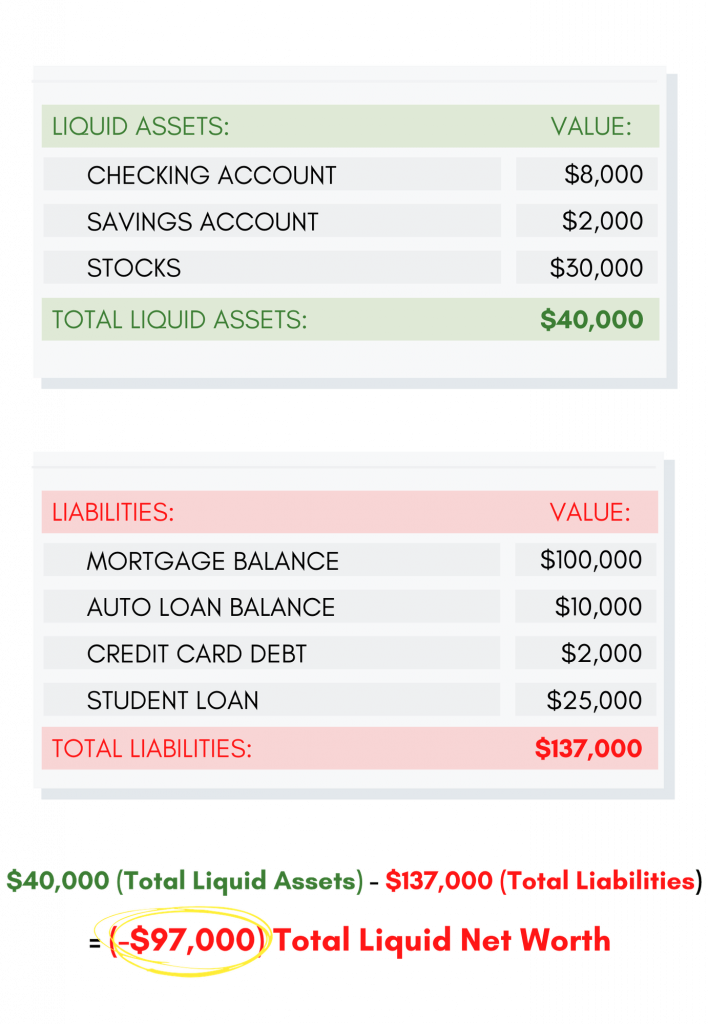

Calculating your liquid net worth is a similar process, but you only need to include your liquid assets and NOT your fixed assets.

Here’s what your liquid net worth calculation would look like:

Yikes!

As you can see, your net worth of $318,000 is substantially different than your liquid net worth, which is a total of negative $97,000.

Why is it negative?

Because in this case, your total liabilities far exceed your liquid assets. This is why it is important to be able to distinguish between the two different types of net worth.

For example, think about when you hear stories of celebrities or famous people going bankrupt. On paper, these people are worth millions of dollars. However, if they have high bills that they need to pay and are unable to quickly come up with the cash then they could find themselves underwater very quickly. They might have 3-4 mansions that are worth several million but these cannot be sold quickly to help cover any liabilities.

How to grow your liquid net worth

If you’ve calculated your liquid net worth and it turned out to be a number that’s not to your liking, don’t worry. There are a couple of ways you can increase your overall net worth as well as liquidity:

1. Grow more income streams

One of the most effective ways to grow your liquid net worth quickly is to increase your active income. You can do this by finding a better-paying job, starting your own business, or getting a second part-time gig or side hustle.

Having multiple streams of income will create more financial stability for you and allow you to build cash savings faster. If you struggle with having any money left over after your bills are paid, you might want to consider finding additional ways to generate income.

The good news is you have endless ways to make more money. You can choose to take on an easy part-time job that pays hourly, or you could offer a service that you have some expertise in and set your own rates.

Whatever you choose, set an income goal that you want to reach every month. Have a dedicated account where you can stash your savings but still have quick and easy access as you grow your liquid net worth.

2. Ask for a raise

Do you feel like you’re being paid what you’re worth? If your answer is no, then it’s time to ask for a raise. Come up with your best argument why your time and skills are worth more than you’re currently getting. Be specific and confident about the increase you wish to receive.

It might benefit you to do a little research before you sit down for the big ask. Find out the average pay range your position currently gets in your area, and even print out your findings to show your boss. Know the qualifications for the higher end of the pay scale so you’re sure you’re justified in your request.

If you *do* feel like you’re getting paid according to your abilities, then maybe it’s time to uplevel your skills. Take the initiative to find out what extra training you need to jump to the next salary level. Let your boss know that you’re motivated to learn more so you can offer more to the company.

Lastly, be prepared to be denied. Know what your next move will be if you don’t get the raise. You’ll need to decide for yourself if there are enough benefits to stay even without a higher paycheck. You may find it’s time to move on to another company that’s willing to pay what you believe you’re worth.

3. Reduce your expenses

Freeing up cash you already make is just as effective as making more. Find those spending leaks that you can minimize or eliminate to have more money available for savings.

The easiest way to do this is to track your spending and stick to a budget. You’ll never have full control of your finances until you have a firm grasp of where your money is going.

I recommend the zero-sum budget method for those who are just starting out with a budget or feel they need more discipline with a spending plan. This strategy makes sure that every dollar is accounted for so you can maximize your income.

Your budget will give you a place to track your spending and see the areas you can cut back on. If increasing your liquid net worth is a financial goal for you, then look at those variable and discretionary expenses to find more ways to save.

Budget categories like dining out, clothing, subscriptions, and monthly memberships are easy areas to reduce spending. But, don’t forget that you can also minimize your necessary expenses by refinancing your mortgage with a better rate, lowering insurance premiums, and avoiding auto loans by driving older vehicles.

When you make your money work more efficiently, you free up income that you’re already making. Find ways to reduce your expenses so you can build cash savings and improve your liquid net worth.

4. Increase your investments

Stocks and bonds are considered liquid assets, so if you want to increase your liquid net worth, start investing more.

With investment vehicles, you will only get the cash once you sell. So, technically speaking, your liquid net worth isn’t affected until you sell and receive capital gains. If you lose money on your investments, your liquid net worth may go down.

Bonds, however, bring guaranteed income. Bonds are also known as fixed assets, which means they provide a stable stream of income (usually paid twice a year).

If you’re not familiar, a bond is money lent to a corporation or government that they promise to repay. In the meantime, they will also pay you for letting them borrow your money.

Bonds have a pre-determined duration before maturity. You will receive a certain amount of fixed income year after year during this duration. Once the bond matures, you’ll receive the principal amount you invested back.

Another fixed income asset that you can use is Certificates of Deposit. These are “less” liquid, in that typically you’re required to keep your money tied up for a specific period of time, unless you want to incur a penalty for early withdrawal.

5. Reduce your debt

You can prioritize the goal of reducing your liabilities by focusing on paying down your debt. Consider putting extra money toward the debt with the highest interest rate. This approach is known as the “avalanche” strategy and helps save a significant amount of money in the long run.

Another effective way to reduce your debt is the “snowball” strategy where you focus on the smallest debt first, and then work your way up to the larger debts. Some people find this much more motivating since it’s easier to see fast results by eliminating the smaller debts quickly.

If this all sounds a bit confusing, consider following these steps to cut down your debt fast:

- Develop a budget to track your expenses – become more aware of your income, and expenses to reduce unnecessary costs.

- Reduce the number of credit cards you have – for the ones you have, make sure they have the lowest interest rates available.

- Pay your bills on time – paying your bills in full and on time will help you avoid late fees and high-interest rates.

- Pay off the debts with the highest interest rates and fees first – this will reduce the amount of money you owe in the long term.

- Get a debt consolidation loan from a credit union or a bank – this will allow you to make only one payment to pay off your debt (instead of several payments to different lenders). Sometimes, you can get a lower interest rate on consolidation.

- Don’t take on more debt – before adding any new debt, work on paying down what you currently owe. You can do this by limiting unnecessary purchases and focusing that income on paying down your debt. It’s a good idea to create your own debt payoff plan or talk to a dedicated and trustworthy credit counselor if you need extra help.

Once you’ve paid off your balances or greatly reduced them, make sure you don’t fall into the debt trap again. Phase out your credit cards if you’re not confident of curbing your excessive spending habit, and start using cash or debit cards instead. That will help you control the urge for unnecessary spending.

Again, following these steps are all dependable ways that you can increase your liquid net worth.

How to track your liquid net worth

It’s wise financial practice to know your liquidity rate. Emergencies tend to pop up unexpectedly, so in order to avoid financial distress, it’s important to be aware of the cash sources you have available to you.

A simple way to track your liquid net worth is with a spreadsheet. You can go digital with Excel or Google Sheets, or be old school with pencil and paper.

The first column of your spreadsheet should be a list of all of your assets that you consider liquid. The next column would be each asset’s individual value. Of course, the values will fluctuate on a daily basis, so just record the most accurate values you can determine today.

If you include assets that require a discounted value, add a third column for the discount rate (typically between 10%-30%) and a fourth column for the net value.

Underneath your assets, either list your liabilities individually, or just enter the grand total.

Finally, just subtract your liabilities from your liquid assets to get your liquid net worth.

Your tracker may look something like this:

As long as your finances don’t drastically fluctuate, updating your liquid net worth once or twice a year should be adequate. Just update the values of your liquid assets and liabilities to see how much your liquid net worth has changed.

The goal is to get to a balance that you feel comfortable with. Have a liquid net worth goal in mind, and make adjustments to your personal finances to achieve it over time.

Why does liquid net worth matter?

While your overall net worth is an important number, it doesn’t indicate your financial freedom or financial stability. That’s what your liquid net worth does.

Your liquidity shows how prepared you are financially to handle unforeseen circumstances or emergencies like job loss, major health expenses, home repairs, car repairs, bigger-than-expected tax bills, etc.

Your liquid net worth can help you cover your expenses without having to sell off your house, car, or other assets at below market value. For a lot of people, high liquidity means financial security as it represents the amount of funds that they can access under short notice.

Need to spend $5,000 to fix your roof? Or maybe you have to travel to the other side of the country for a death in the family? What if you have to undergo emergency gallbladder removal surgery and stay in the hospital for a week?

Any one of these out-of-the-blue expenses can be devastating for those who live paycheck-to-paycheck or have little to no liquidity. Unfortunately, the number of people living in these types of situations has increased since the COVID-19 virus swept through America. This is why it’s important to keep an eye on your liquid net worth and take every measure you can to grow it.

Other important financial metrics to track

Financial metrics are quick and simple indicators of your progress toward achieving your financial goals. And, while your net worth is an effective measure of your overall wealth, there are several other metrics you should be tracking on your way to retirement.

Besides your net worth, I recommend keeping an eye on these 4 financial metrics to gauge your retirement readiness:

- Financial independence number – This metric represents the net worth you’ll need to accumulate in order to be financially independent and completely live off of savings. The factors that impact your FI number are your projected annual retirement spending and the withdrawal rate you’ll apply to your retirement savings.

- Savings rate – this personal finance ratio specifies the percentage rate of your income that you save in a certain period of time. Many financial advisors recommend that you maintain a savings rate of at least 15% once you turn 25. If you’re a late saver, your savings rate will need to be higher if you want to retire on time.

- DTI ratio – DTI stands for Debt-To-Income, and will inform you of how well you’re paying down your debts. The higher your DTI, the more you need to make debt payoff a priority. Financial lenders will often look for a DTI of 30% or lower, but your goal should be to minimize this metric and get it as close to zero by the time you retire.

- Liquidity ratio – Just like liquid net worth, your liquidity ratio is a helpful reflection of your financial security. Except, instead of measuring in dollars, this metric measures time and indicates how long you can be supported solely by your liquid assets.

These personal finance ratios are explained further in my post about metrics to follow for retirement planning. Check it out to learn how to calculate each one and how they can help you prepare for retirement. You can even get a free monthly metric tracker to download.

Don’t forget to download this FREE Monthly Metric Tracker to track 4 important metrics for your retirement planning!

Final thoughts on liquid net worth

I think we would all like to experience more security with our finances, and a simple way to assess where you’re at is by calculating your liquid net worth.

This important metric will help you prepare to meet unexpected expenses and emergency situations without crippling your retirement plans and derailing your budget.

Keeping a good handle on your liquidity will serve you well in strengthening your future financial health.

Other posts you may enjoy:

- 51 Money-Saving Challenges for 2021

- $40,000 A Year Is How Much An Hour?

- How To Make A Six-Figure Salary

- How To Build A 6-Month Emergency Fund In 5 Simple Steps

- 50+ Easy Ways To Make Extra Money

- How To Create Your Budget Categories

- 3 Reasons To Not Use Savings To Pay Off Debt

- How To Live On Last Month’s Income (And Why You Should)

- How To Live Within Your Means (And Still Be Content)

- Financial Health Checkup: 7 Steps To Boost Your Fiscal Well-being

Want to remember this post for later? Pin it to your favorite Pinterest board!