If looking at your budget brings you down, perhaps you need to take a break from it and look at your financial situation from a different angle. One way to do that is to calculate net worth.

I’m sure you would agree that managing a budget is not the most exciting thing in the world to do.

In fact, at times it can be downright frustrating. You might even feel like you’re spinning your wheels.

Maybe you can only pay the minimum on your credit card balance. Or just as soon as you get some breathing space an unexpected expense comes up.

I totally get it, because I’m right there with ya! Sometimes I want to throw the budget out the window and just wing it, because it doesn’t seem like saving $7.45 at the grocery store is making much of a difference.

Fortunately, the state and impact of your monthly budget doesn’t define your long term financial goals. In fact, there are some people that have eliminated keeping a budget altogether. Instead, they utilize a high-level metric to keep them on track. Rather than focusing on the daily management of income, they calculate net worth to get a better view of their overall financial picture.

A budget helps you track the small daily choices you make to manage your income. It’s like a macro lens, allowing you to see the smallest money movements.

Your net worth is more like a wide angle lens. It gives you a broad perspective of your finances to help you make better decisions for building wealth.

It’s simple to learn how to calculate net worth, but let’s walk through the steps together.

Table of Contents

How to calculate net worth

Knowing what net worth is will help you understand how to find yours.

In basic terms, your net worth is the difference between what you owe and what you own.

What you owe is called your liabilities, and what you own is called your assets.

If the total of your assets is greater than the total of your liabilities, you’ll have a positive net worth. Conversely, if your liabilities are greater than your assets, your net worth will be negative.

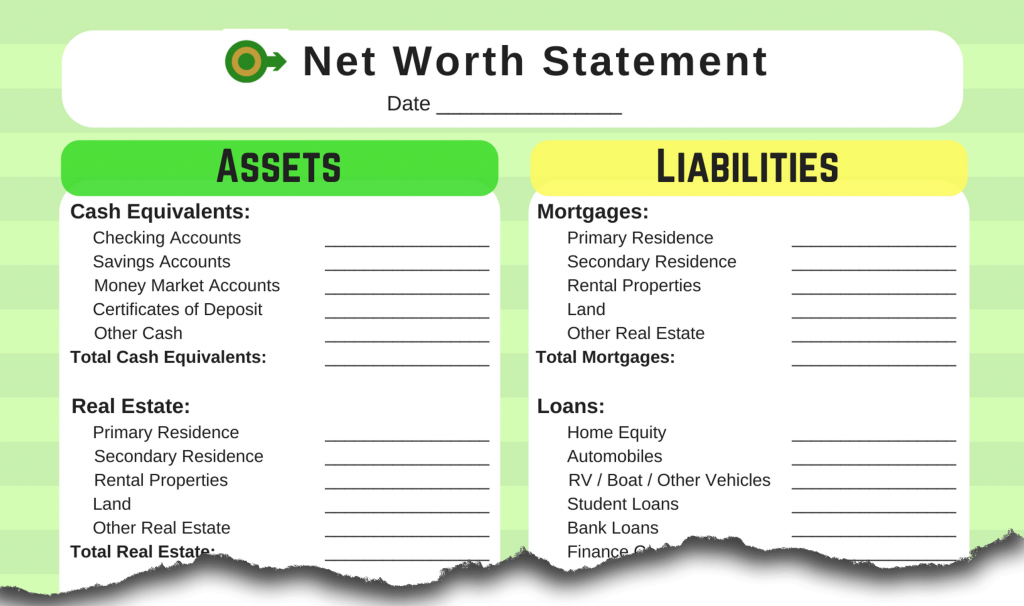

ASSETS COULD INCLUDE:

- Your home and other real estate properties

- All types of vehicles

- Investments and retirement accounts

- Your checking and savings accounts

LIABILITIES MIGHT BE:

- Mortgages

- Auto loans

- Credit card balances

- Student loans

And just to make a distinction:

You own your home, but you owe a mortgage.

You own a car, but you owe an auto loan.

Unfortunately our vehicles depreciate significantly as the interest keeps accumulating on our car loans. This can cause your car to contribute negatively to your net worth.

However, your home (hopefully) has increased in value if you’ve lived in it for some time. You’ll want to add that additional equity to your net worth.

You will need to estimate these values by using resources such as Kelly Blue Book for your vehicles and Zillow for your properties. If you want to include the value of personal items such as jewelry or collectibles, see what bidders are willing to pay for them on eBay.

Once you have totals for both assets and liabilities, just subtract to find your net worth.

TOTAL ASSETS – TOTAL LIABILITIES = NET WORTH

How to calculate net worth: an example

Let’s say Bob is an architect making an annual salary of $85,000. He’s lived comfortably in the suburbs for about 8 years in a beautiful home with his wife and kids. His house has gained some value but he still has a mortgage on it. He has two vehicles parked in his garage, one is paid off and the other has a loan. He’s been faithfully putting money in his company’s 401K and building up his savings account, but he does have some credit card debt and student loans. Here is what Bob’s net worth statement would look like:

ASSETS

Home’s current value: $350,000

Vehicle 1 current value: $10,000

Vehicle 2 current value: $8,500

Checking & Savings Account balances: $7,500

401(k): $65,000

Total Assets: $441,000

LIABILITIES

Mortgage balance: $245,000

Auto loan: $5,500

Credit cards: $8,500

Student Loans: $35,000

Total Liabilities: $294,000

Bob’s net worth would be: $441,000 – $294,000 = $147,000

If you went to visit Bob you may think he’s doing really well, but when you step back and look at the overall picture it’s really not that impressive. His net worth is less than two years of his annual salary.

This is the cold, hard truth of net worth. It tells you the bottom line of where you’re at today.

The good (and bad) news is it will be different next month, and that’s why it’s important to track it.

Why it’s important to calculate net worth

Your net worth is like a report card that lets you know how well you’ve been doing with your finances since your very first paycheck. Every time you calculate it you see a snapshot of your financial situation at that particular moment in time.

Finding your net worth can either be like a splash of cold water in the face, or a congratulatory pat on the back, depending on how well you’ve been handling your money.

But regardless of how you feel after you see your number, knowing your net worth is imperative in helping you reach your financial goals. Tracking it will help you identify areas where you’re overspending and inspire you to be more purposeful in saving.

As you review changes in your assets and liabilities over time, you’ll become more aware of how to best use your money in order to increase wealth.

For example, you may decide to sell one of your cars to pay off an auto loan and use the amount left over to buy a cheaper vehicle. Or you may realize that you should use some of your savings in that low interest bearing account to pay off that high interest credit card debt.

You may be wondering how often you should calculate your net worth. Because your situation is unique to everybody else’s, that will be a personal decision that works best for you. Some people like to track it weekly, others monthly, and some quarterly or even yearly. The important thing is to keep tracking it.

It’s important to remember that your net worth will constantly fluctuate as you continue to pay down debt and increase savings. So it’s not the number that matters most, but the overall trend in which it moves.

What should your net worth be?

If you want to experience financial freedom, your goal is to consistently increase your net worth. But depending on your income and your cost of living, your net worth goal won’t be the same as someone in a different profession and living in another state.

There are benchmarks that have been created, such as the classic formula from the book The Millionaire Next Door by Stanley & Danko. It’s best for those who are over 40, have been in the workforce for a couple decades, and have a steady income. The calculation looks like this:

(Age x Annual Pre-tax income) / 10

You can also use a net worth calculator, such as the one on CNN Money. This particular one only accounts for income OR age, not both. Still, it gives you an idea where you stand compared to the median for both factors.

It’s helpful to know how your net worth compares to these benchmarks, but just remember the most important standard you should compare yourself to is you. With any clever formula or calculation there will always be variables missing that directly apply to you. That’s why the one true benchmark for your own net worth is what it was last month, or last year, or 3 years ago. Your life circumstances may change and your number will fluctuate, but over time, year after year, your net worth should be increasing.

Net worth tracking tools

You really only need a pencil and a piece of paper to calculate net worth. (And a calculator, if you don’t trust your math). But if you plan on tracking your number consistently, it’s helpful to have some good tools. A worksheet, a spreadsheet, or an online resource can help you save time with organizing and calculating.

If you like the feeling of a pencil in your hand, you can download this net worth worksheet that I created.

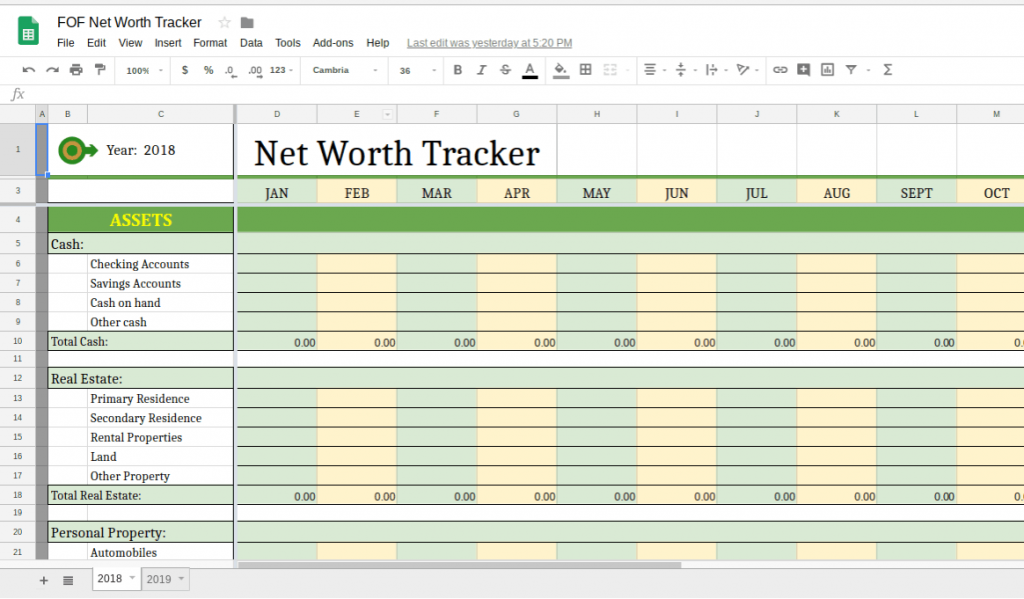

Or if you’d rather have your fingers on a keyboard, download a copy of this Google Sheets spreadsheet that I also designed and use to calculate my own net worth.

Lastly, if you prefer completely automated and real time tracking with cool graphs, sign up for a Personal Capital account. It’s free!

In conclusion

If you’re ready to improve your financial health, first find out how well it’s doing by calculating your net worth. Let that number inspire you to get serious about increasing your wealth, and then track it on a consistent basis. Besides, it’s a nice break from your fussy budget, and you may be pleasantly surprised that seeing the big picture can provide you with the motivation you need to keep making those small daily choices.

Do you already track your net worth? Or have you been putting it off because the truth might hurt? Leave a comment below and let me know how you use this metric to help you build wealth!

Other posts you may be interested in:

- How To Save $5000 In A Year

- 11 Effective Ways To Stay Motivated With Your Goals

- The Purpose Of A Budget: 17 Powerful Benefits

- 3 Smart Reasons To Put Savings Before Debt

- How To Live On Last Month’s Income (and Why You Should)

- 14 (Mostly Free) Online Money Management Tools

- How To Live Within Your Means (and Still Be Content)

- Financial Health Checkup: 7 Steps To Boost Your Fiscal Well-being

- How To Escape Debt With A DIY Debt Management Plan

- The Zero-Sum Budget Resource Guide