Table of Contents

FPU Lesson 6: Dave Ramsey’s Insurance Advice

(This post is part of my Finance Peace University Review series from 2019, and updated in 2020 with additional content!)

This review covers the 6th lesson in Dave Ramsey’s Financial Peace University Flex online course.

The previous lessons are covered in these posts:

- Week 1: Starting an Emergency Fund & Budgeting (Baby Step 1)

- Week 2: How to pay off debt using the Debt Snowball method (Baby Step 2)

- Week 3: How to build up a fully-funded 3 to 6-month emergency fund (Baby Step 3)

- Week 4: Retirement, homeownership, college, and building wealth (Baby Steps 4-7)

- Week 5: How to spend wisely and protect your wealth

Financial Peace University “Flex” is the online version of Dave Ramsey’s popular personal finance course.

Instead of meeting in person, in small groups, on a weekly basis, the curriculum is provided entirely online. This includes Financial Peace videos, worksheets, and even an online community for additional support.

The 9-week course teaches money management strategies like budgeting, debt payoff, and financial planning.

I learned a lot going through this series on my own. Each video provides a worksheet to help you follow along and take notes, and each session has a checklist so you can stay on track with the program.

I’ve written a review for each of the 9 videos (as well as a bonus “Top 10 Lessons”), and I hope it helps you get better control over your own money management.

In this review of the Financial Peace University Week 6 lesson, I share Dave Ramsey’s insurance advice, and his recommendations for how to build a strong defensive game plan for your wealth.

When should I transfer risk?

Sometimes, insurance can seem like a waste of money. After all, you pay all those monthly premiums without knowing if you’ll ever get any benefit in return.

But, without it, you take on the risk of getting slammed with hospital bills or auto repair costs.

The reason people buy insurance is to transfer risk. The “risk” is the financial liability for an unfortunate life event that may or may not happen.

In other words, you’re buying protection against a financial crisis.

There are lots of small financial risks you could take on yourself, like handling a flat tire or the flu. If you’ve done the baby steps, then you’re in a position to take care of these issues without getting an insurance company involved.

But, when you’ve totaled your car, or you’ve been diagnosed with cancer – then you need to be covered so you don’t end up with a financial crisis.

You should only pay insurance premiums for those big risks that you’re unable to take on yourself. This will protect you from the danger of going bankrupt and losing everything you’ve worked so hard for.

This lesson in the course teaches us that certain insurance policies will protect you, while others take advantage of you.

The key is in knowing the difference and choosing wisely.

Dave’s advice for auto insurance

Like I already mentioned, if you’ve done the work and have set yourself up for a solid financial future, then you are able to take on some risk yourself. This can mean lower premiums for you.

For example, if you have a 6-month emergency fund, you’re out of debt, and you’re building wealth, then you can safely increase your deductible on your auto insurance.

Basically, you pay the insurance company less because you’re taking on more risk yourself.

However, there is a point where the higher deductible is not worth it. That’s why it’s important to do a break-even analysis to determine how much higher you can go and still have an acceptable outcome.

Also, make sure you have adequate liability coverage. Personal liability covers any bodily injury and property damage sustained by other people for which you’re responsible. It’s also the best buy you’ll find in insurance – the cost is minimal but the protection is invaluable.

You do not want to mess around with this. Check your liability coverage TODAY! Dave highly recommends a minimum of $500,000 in liability coverage.

Lastly, if you have an older car and have a large emergency fund, you can consider dropping collision. This coverage is for fixing your own car after a wreck.

However, the cost has become very affordable, so check your rates and make the decision that’s best for you. (If you don’t have a large emergency fund, then keep the collision coverage. Otherwise, you could be hoofin’ it.)

Related Post: How To Build A 6-Month Emergency Fund In 5 Simple Steps

Dave’s suggestions for homeowner’s insurance

Dave mentions two types of homeowner’s insurance: guaranteed replacement cost and extended replacement cost.

Guaranteed replacement cost covers the cost of rebuilding your home exactly as it was before the damage, even if the cost is greater than the actual value of the home.

This protects you from sudden increases in construction costs, which is common after a natural disaster when many claims are submitted. This is the coverage that Dave recommends.

Extended replacement cost covers an additional 20-25% of the replacement value of the home. This coverage is easier to find and is more common for properties valued under $500K.

It’s important to keep this type of policy updated with the current value of your home so you don’t lose money if the value has appreciated.

Once you’ve built up a substantial retirement fund and have a good amount of equity in your home, Dave highly recommends an umbrella policy. He calls it a “great buy” that gives up to an additional $1 million in coverage for only $200-$300 a year.

Dave’s tips for health insurance

Dave reports that the #1 reason for bankruptcy in America is due to either the type of health insurance people have, or not having any at all.

High-deductible, 80/20 plans can result in a mountain of medical bills that leave people on the brink of financial disaster if they don’t have a healthy emergency fund.

This is why it is *so* important to build up your savings.

And, when you have reached a good level of financial security, you have the option of increasing your deductible so your premiums are lower. Let your emergency fund cover the smaller medical issues, and leave the big stuff to the insurance companies.

One number you need to know is your stop-loss. This is the amount of out-of-pocket expenses you need to pay before the insurance company picks up 100% of the tab.

Dave recommends not changing this number to save some money – but it’s important that you know what it is.

One feature you should never decrease in order to lower your premium is the maximum pay. This is the maximum amount the insurance company is willing to cover. It’s never worth it to lower this amount just so you can save a few bucks.

If you don’t currently have an HSA (Health Savings Account), look into it and see if it’s right for you and your family. There are some great benefits to it, but only if you’re on either side of the spectrum – really healthy, or really sick.

If you tend to pay a good part of your deductible but never quite reach the maximum, then an HSA probably won’t be a good addition to your coverage.

However, if you are someone who either rarely uses your coverage or tends to pay 100% of your deductible, then the HSA is a wise choice.

We get our health insurance through my husband’s employer and we currently have an HSA. We’ve had high medical bills for the past couple years and this plan has saved us so much money. I cannot even *begin* to tell you how thankful I am for it!

You may need to increase your disability coverage

Disability insurance will partially replace your income if you can’t work due to a short-term or permanent disability.

Most people will underestimate their chances of needing disability coverage, but in fact, 30% of Americans will experience a permanent disability in their lifetime!

Dave tells us that this is the most under-insured area in a financial plan, and yet it is crucial to your defensive strategy.

Again, one of the reasons for having a large emergency fund is so you can handle the smaller emergencies that arise. But, when you lose your ability to generate an income, you’re going to need an insurance policy to carry you beyond what your emergency fund can do.

If you have enough in the bank to cover you for a little while, then you can skip the short-term disability. You’ll need to look at your financial situation and determine if this is a wise choice for you.

However, unless you’ve got millions in the bank, everyone needs long-term disability.

The cheapest place to get it is through your work, but if that’s not an option then check any trade association you’re connected to. Your last option is going through an insurance agent, just make sure they work for an independent broker and not for a particular brand.

A specific type of disability is occupational, or “own-occ” insurance. This type of policy will cover you when you cannot perform the job you were educated or trained to do.

So, if you were trained to be a dancer and you get in an accident that leaves you in a wheelchair, then this insurance would be super helpful.

However, it typically won’t cover your entire life. After a couple of years raking in the insurance checks while you sit on the couch watching Dancing with the Stars, your insurance company will cut off the money and tell you to go find another line of work.

A few tips from Dave about disability insurance:

- Don’t even consider policies that cover less than 5 years.

- If you get your LTD through work, always buy with after-tax income – otherwise, your LTD checks will be taxed

- be prepared to make adjustments in your budget if you’re on LTD, because it will typically cover only 50-65% of your current income.

- To lower your premium, opt for a longer elimination period. This is considered the deductible, and it’s the time between being declared by your doctor that you are disabled and when you receive your first LTD check. This is typically 90 days, but you can choose 180 days to lower your premium and save some money.

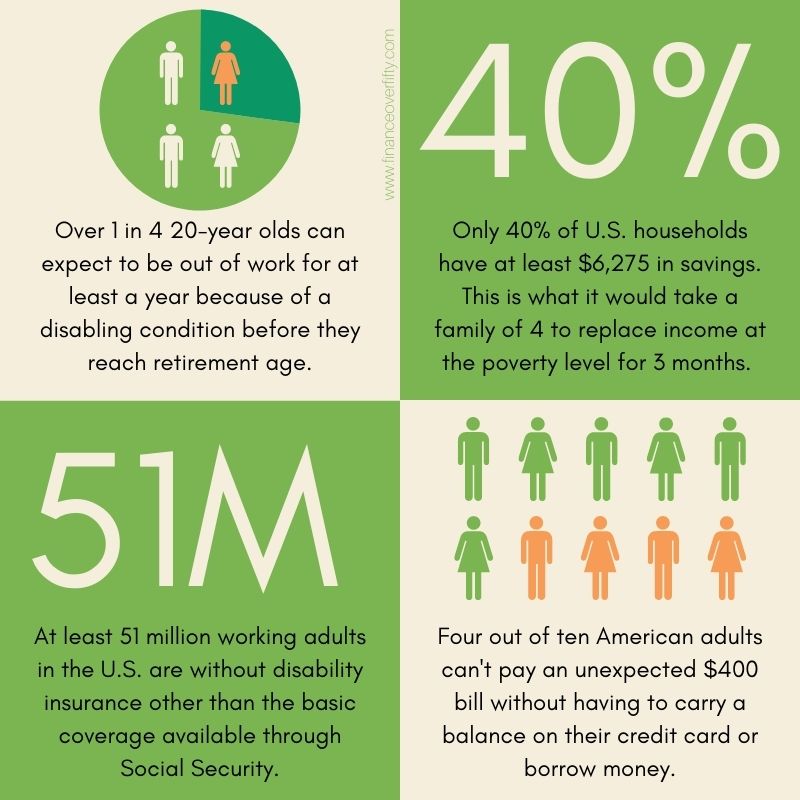

Infographic: Disability Risk in America

Resource: CDA 2019 Disability Awareness Survey

Over 60? You need long-term care

This type of insurance is an absolute must if you’re over 60.

It will cover nursing homes, assisted living facilities, and in-home care. These are expenses that you do not want to leave to your children. (Remember – you want to be a blessing, not a burden.)

Dave says this coverage is basically useless before you’re 60 because statistically you only have a 1% chance of needing these services before then.

And this isn’t just for the person needing the care. It’s just as much for the healthy spouse who may end up a widow.

You don’t want to leave your husband or wife in a situation where the entire nest egg was used up taking care of you and he or she is left behind with nothing.

These are tough things to think about, but it’s a part of reality. Show your family how much you love them by getting these things in place before it’s too late.

Protect your identity

Identity theft protection is not technically insurance, because when your identity is stolen there is no loss of income or ability. You are never liable for money that was stolen from you.

However, restoring your identity with all of your creditors is a complicated, messy, annoying and awful process that’s a huge time-sucker.

Do yourself a favor and get this protection. Pay someone else to clean up the mess so you know it’s been done thoroughly and you can get back to your regular life as soon as possible.

*Dave tip: do not buy protection that only provides credit report monitoring – you can do this yourself (easily) for free.

Do you really need life insurance?

The only reason my husband and I have life insurance is because our friend started selling it when we were expecting our second child and we thought it was a good idea (and we wanted to help our friend).

After listening to Dave in this lesson, I realized it might be wise to either decrease the policy or eventually get rid of it altogether.

This is because once you’re completely out of debt and you have some wealth built up, you can insure yourself. We’re not in this position yet, but it’s nice to know that when we are we can drop the premium.

The two types that Dave talks about are term and cash value life insurance.

Term is for a specified period of time, is the cheaper of the two, and has no savings plan built in.

Cash value is normally for life, is more expensive, and does have a savings plan built in. This sounds good, but if you read the fine print you’ll find out that the rate of return is horribly low, and – AND – when you die, anything left in savings goes back to the insurance company. Crazy, right?

Dave calls this a ripoff, and he highly recommends firing your agent if they suggest you buy cash value life insurance.

So, best to stick with term, get enough to cover 10 years of your income, and put the cost difference between term and cash value into mutual funds that will give you returns that are much higher.

Video: Why Whole Life Insurance Sucks!

Which insurance to avoid

Here are types of insurance that Dave says to skip:

- Credit life & Credit disability

- Cancer and hospital indemnity policies

- Accidental death

- Pre-paid burial

- Mortgage life

You’d do better to put the money it would take to cover premiums into mutual funds.

Don’t forget a will

This is so important, yet so many people put it off!

Get a written will – either do it yourself online or pay for a lawyer.

My husband and I do have a will, but admittedly we need to get it updated. I’m leaning towards shelling out the money for a lawyer so I know it’s legit and complete.

Dave suggests having a legacy drawer in your home. Put all your insurance documents, estate plans, your written will, instructions, phone numbers, letters, and everything else that your loved ones will need when the time comes.

Making sure that everything is taken care of and organized shows your family you love them and gives you a whole new layer of financial peace.

Related Post: Ultimate Estate Planning Checklist & Guide

What’s next

The next stop on this Financial Peace journey is retirement planning, which is essentially wealth building. This will mainly be about how to invest your money the smart way.

Going through this course has been so helpful, but also has gotten me excited about retirement!

We have a ways to go, but just knowing we have so much to look forward to if we follow the plan gives me a sense of hope, anticipation, and security.

You really can take back control of your money and your life and fulfill the dreams you have for yourself and for your family. It will take sacrifice, focus, and intention, but it will be so worth it in the end.

I’m all in, how ’bout you?

Other posts you may enjoy:

- Pros and Cons of a Health Savings Account

- The 401(k) and the IRA: Which One Is Better?

- The Late Starter’s Essential Roadmap For Retirement

- Ultimate Estate Planning Checklist & Guide

- Get Your RISE Score: 5 Steps To Determine Retirement Readiness

- Should You Use The 4% Rule In Retirement?

- 7 Steps To Catch Up On Retirement Savings

- 12 Effective Tips For Financial Planning In Your 50s

- 50 Good Money Habits To Help You Save More

- What Happens If You Don’t Have A Living Trust?